Abstract

The recession of the early 1990s caused a serious unemployment problem in Finland. This study investigates the role of compositional variation in unemployment duration using individual data on Finnish workers. The compositional effect is examined by predicting the impact of the observed unemployment inflow heterogeneity on aggregate re-employment rates. Focusing on a recession period provides useful variation for the analysis due to large increase in the unemployment inflow. According to the results, the aggregate outflow effect dominates and the observed compositional variation implies only a small increasing trend in the average duration during the recession period.

Similar content being viewed by others

Notes

The long-term unemployment rate is the main macroeconomic indicator that is related to unemployment duration. Individuals are defined as long-term unemployed after 12 months of unemployment.

The conditions of the earnings-related allowance changed only slightly during the 1990s and the replacement rates remained relatively stable. The required number of months in work was raised from 6 to 10 months in 1997.

This rule came into effect first in 1996 for those under 20 years of age but it was extended for those under 25 in 1997.

Some individuals have consecutive unemployment spells with short breaks between them. The spells are joined in the analysis data if the breaks are shorter than 20 days.

Loess is a local regression method proposed by Cleveland (1979).

The exits to unknown state are not strongly related to the duration of spell. The main results of the compositional analysis are robust to treating the exits to unknown state as censored observations.

To assess the robustness of the results, a mixed proportional hazard model was estimated. Extending the model up to three mass points for the unobserved heterogeneity changes the parameter estimates. However, the main impact is on the baseline hazard and this extension gives qualitatively similar results for the compositional variation as the main model.

References

Abbring J, van den Berg G, van Ours J (2001) Business cycles and compositional variation in U.S. unemployment. J Business Econ Stat 19(4):436–448

Abbring J, van den Berg G, van Ours J (2002) The anatomy of unemployment dynamics. Eur Econ Rev 46:1785–1824

Baker M (1992) Unemployment duration: compositional effects and cyclical variability. Am Econ Rev 82:313–321

Cleveland WS (1979) Robust locally weighted regression and smoothing scatterplots. J Am Stat Assoc 74:829–836

Darby M, Haltiwanger J, Plant M (1985) Unemployment rate dynamics and persistent unemployment under rational expectations. Am Econ Rev 75(4):614–637

Dejemeppe M (2005) A complete decomposition of unemployment dynamics using longitudinal grouped duration data. Oxf Bull Econ Stat 67(1):47–70

Elsby M, Michaels R, Solon G (2009) The ins and outs of cyclical unemployment. Am Econ J Macroecon 1(1):84–110

Heckman J, Singer B (1984) A method for minimizing the impact of distributional assumptions in econometric models for duration data. Econometrica 52(2):271–320

Honkapohja S, Koskela E (1999) The economic crisis of the 1990s in Finland. Econ Policy 14(29):399–436

Imbens G, Lynch L (2006) Re-employment probabilities over the business cycle. Portuguese Econ J 5(2):111–134

Koskela E, Uusitalo R (2006) Unintended convergence: how Finnish unemployment reached the European level. In: Werding M (ed) Structural unemployment in Western Europe: reasons and remedies. MIT Press, Cambridge

Kyyrä T, Wilke R (2007) Reduction in the long-term unemployment of the elderly: a success story from Finland. J Eur Econ Assoc 5(1):154–182

Rosholm M (2001) Cyclical variations in unemployment duration. J Popul Econ 14:173–191

Shimer R (2007) Reassessing the ins and outs of unemployment. NBER Working Papers

Turon H (2003) Inflow composition, duration dependence and their impact on the unemployment outflow rate. Oxf Bull Econ Stat 65(1):31–47

Wooldridge JM (2002) Econometric analysis of cross section and panel data. MIT Press, Cambridge

Acknowledgments

I thank Per Johansson, Roope Uusitalo, Tuomas Pekkarinen and Tomi Kyyrä for their helpful comments. I am also very grateful to Tomi Kyyrä for providing the R routines for the estimation of mixed proportional hazard models. Yrjö Jahnsson Foundation is acknowledged for the financial support.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

See Tables 1, 2, 3, 4 and Fig. 5.

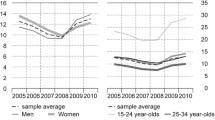

Seasonally adjusted regional and aggregate (solid line) unemployment rate series (source: Labour Force Survey, adjusted for definition change in 1997 due to EU standards)

Rights and permissions

About this article

Cite this article

Verho, J. Unemployment duration and the role of compositional variation: evidence from a period of economic crisis in Finland. Empir Econ 47, 35–56 (2014). https://doi.org/10.1007/s00181-013-0732-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-013-0732-3