Abstract

This paper investigates the cyclicality of research and development (R&D) activities during the Great Recession period by incorporating the role of credit constraints, using the Great Recession period as a natural case study. Recession period is a good setting in which to identify cyclicality and eliminate endogeneity issues that have been discussed in the literature. Using firm-level data on non-federally funded, high-technology firms in the USA, this paper shows that firms without bond ratings had more procyclical R&D investments than those firms with bond ratings. I also test whether capital or inventory investments of firms that also do R&D are procyclical. I find that firms without bond ratings adjust their inventories more rapidly compared to capital and R&D investments, when they are hit by a bad shock.

Similar content being viewed by others

Notes

See Hall and Lerner (2010) for a detailed discussion of financing of R&D and a review of the literature related to financial constraints on R&D investment.

See Erickson and Whited (2000) on measurement error problems in Tobin’s Q.

For this analysis, I construct capital stock series for each firm, using the perpetual inventory method and capital expenditures data. Inventory stock data are available on the Compustat database.

See Arvanitis and Woerter (2013) for a good summary of theories in this literature.

These results are in line with Brown et al. (2009).

Using the data from National Science Foundation, Anzoategui et al. (2016) show that R&D expenditure per capita of the US corporations experienced a sharper contraction before and during the 2001–2002 crisis than the Great Recession period. Bianchi et al. (2014) find during the Great Recession, there was a significant drop in technology adoption and utilization rates, but small change in accumulation of knowledge. In contrast, during 2001 there was a modest change in the adoption rate of technology. They conclude that the aforementioned characteristics of the Great Recession resulted in severe contractions in the short-term, but had less effect on the trend growth.

The list of non-federally funded, high-tech industries was obtained from Brown et al. (2009).

This fact is well documented by Brown et al. (2009).

The steps that I take in constructing the regression sample are explained in detail in “Appendix”.

See Hall and Lerner (2010) for a discussion of why there is often a large wedge between internal and external sources of finance for R&D investments compared to other types of investments.

Kashyap et al. (1994) apply this step before they test for the liquidity constraints on the inventory investment of the firms.

I apply this rule because due to small sample size there are very few firms without access to bond markets, and the estimation does not have enough statistical power with the previous definitions of \(B=1\) and \(B=0\).

Eberly et al. (2008) is an example of research that uses double-declining balance.

I used the FRED (Federal Reserve Economic Data) database from the Federal Reserve Bank of St. Louis to assemble the data used herein; see the references for information on the specific series.

I used the FRED (Federal Reserve Economic Data) database from the Federal Reserve Bank of St. Louis to assemble the data used herein; see the references for information on the specific series.

Some studies in the literature suggest taking a constant growth rate that applies to all firms, which is around 5 or 8% (Hall 1990, 1993; Hall and Mairesse 1995). Hall and Mairesse (1995) point out that the choice of growth rate has an effect on the initial stock, but it declines in importance as time passes. More recent studies choose growth rates that differ at the firm or industry level (Parisi et al. 2002; Lyandres and Palazzo 2012). In this paper, the main results are obtained by using different growth rates at the industry level. The results, obtained by using a fixed growth rate, are also reported as a robustness check.

I used the FRED (Federal Reserve Economic Data) database from the Federal Reserve Bank of St. Louis to assemble the data used herein; see the references for information on the specific series.

I used the Organization for Economic Co-operation and Development (OECD) database to assemble the data used herein; see the references for information on the specific series.

References

Aghion P, Saint-Paul G (1998) Virtues of bad times interaction between productivity growth and economic fluctuations. Macroecon Dyn 2(3):322–344

Aghion P, Angeletos GM, Banerjee A, Manova K (2005a) Volatility and growth: credit constraints and prodcutivity-enhancing investment. NBER Working Paper 11349

Aghion P, Bloom N, Blundell R, Griffith R, Howitt P (2005b) Competition and innovation: an inverted-u relationship. Q J Econ 120(2):701–728

Aghion P, Askenazy P, Berman N, Cette G, Eymard L (2012) Credit constraints and the cyclicality of R&D investment: evidence from France. J Eur Econ Assoc 10(5):1001–1024

Aghion P, Akcigit U, Howitt P (2014) What do we learn from Schumpeterian growth theory? Handb Econ Growth 2:515–563

Almeida H, Campello M (2007) Financial constraints, asset tangibility, and corporate investment. Rev Financ Stud 20(5):1429–1460

Alti A (2003) How sensitive is investment to cash flow when financing is frictionless? J Finance 58(2):707–722

Anzoategui D, Comin D, Gertler M, Martinez J (2016) Endogenous technology adoption and R&D as sources of business cycle persistence. NBER Working Paper 22005

Arvanitis S, Woerter M (2013) Firm characteristics and the cyclicality of R&D investments. Ind Corp Change 23(5):1141–1169

Barlevy G (2007) On the cyclicality of research and development. Am Econ Rev 97(4):1131–1164

Bernanke B, Gertler M (1989) Agency costs, net worth, and business fluctuations. Am Econ Rev 79(4):14–31

Bianchi F, Kung H, Morales G (2014) Growth, slowdowns, and recoveries. NBER Working Paper No w20725. Available at SSRN: https://ssrn.com/abstract=2535177

Brown JR, Petersen BC (2009) Why has the investment-cash flow sensitivity declined so sharply? Rising R&D and equity market developments. J Bank Finance 33(5):971–984

Brown JR, Petersen BC (2011) Cash holdings and R&D smoothing. J Corp Finance 17(3):694–709

Brown JR, Petersen BC (2015) Which investments do firms protect? Liquidity management and real adjustments when access to finance falls sharply. J Financ Intermed 24(4):441–465

Brown JR, Fazzari SM, Petersen BC (2009) Financing innovation and growth: cash flow, external equity, and the 1990s R&D boom. J Finance 64(1):151–185

Brown JR, Martinsson G, Petersen BC (2012) Do financing constraints matter for R&D? Eur Econ Rev 56(8):1512–1529

Cincera M, Cozza C, Tübke A, Voigt P (2012) Doing R&D or not (in a crisis), that is the question. Eur Plan Stud 20(9):1525–1547

Eberly J, Rebelo S, Vincent N (2008) Investment and value: a neoclassical benchmark. NBER Working Paper 13886

Erickson T, Whited TM (2000) Measurement error and the relationship between investment and q. J Polit Econ 108(5):1027–1057

Fazzari SM, Hubbard RG, Petersen BC, Blinder AS, Poterba JM (1988) Financing constraints and corporate investment. Brook Pap Econ Activity 1:141–206

FRED (Federal Reserve Economic Data) Data source: Federal Reserve Bank of St. Louis:. Gross Domestic Product: Implicit Price Deflator [GDPDEF]; Gross private domestic investment: Fixed investment: Nonresidential (implicit price deflator) [A008RD3Q086SBEA]; US Department of Commerce: Bureau of Economic Analysis http://research.stlouisfed.org/fred2/series

Gilchrist S, Himmelberg CP (1995) Evidence on the role of cash flow for investment. J Monet Econ 36(3):541–572

Hall BH (1990) The manufacturing sector master file: 1959–1987. NBER Working Papers 3366

Hall BH (1993) The stock market’s valuation of R&D investment during the 1980’s. Am Econ Rev 83(2):259–264

Hall BH, Lerner J (2010) The financing of R&D and innovation. Handb Econ Innov 1:609–639

Hall BH, Mairesse J (1995) Exploring the relationship between R&D and productivity in French manufacturing firms. J Econom 65(1):263–293

Hall BH, Mairesse J, Branstetter L, Crepon B (1998) Does cash flow cause investment and R&D? An exploration using panel data for French, Japanese, and United States scientific firms. IFS Paper No W98/11; Nuffield College Paper No 142; Berkeley Dept of Economics Paper No 98-260. Available at SSRN: https://ssrn.com/abstract=105089 or http://dx.doi.org/102139/ssrn105089

Hall BH, Jaffe A, Trajtenberg M (2005) Market value and patent citations. RAND J Econ 36(1):16–38

Hennessy CA, Whited TM (2007) How costly is external financing? Evidence from a structural estimation. J Finance 62(4):1705–1745

Himmelberg CP, Petersen BC (1994) R&D and internal finance: a panel study of small firms in high-tech industries. Rev Econ Stat 1:38–51

Hoshi T, Kashyap A, Scharfstein D (1991) Corporate structure, liquidity, and investment: evidence from Japanese industrial groups. Q J Econ 106(1):33–60

Hubbard RG (1998) Capital-market imperfections and investment. J Econ Lit 36(1):193

Kaplan SN, Zingales L (1997) Do investment-cash flow sensitivities provide useful measures of financing constraints? Q J Econ 112(1):169–215

Kashyap AK, Lamont OA, Stein JC (1994) Credit conditions and the cyclical behavior of inventories. Q J Econ 109(3):565–592

Lamont O (1997) Cash flow and investment: evidence from internal capital markets. J Finance 52(1):83–109

López-García P, Montero JM, Moral-Benito E (2013) Business cycles and investment in productivity-enhancing activities: evidence from Spanish firms. Ind Innov 20(7):611–636

Lyandres E, Palazzo B (2012) Strategic cash holdings and R&D competition: theory and evidence. Available at SSRN 2017222

OECD (Organization for Economic Co-operation and Development) Data source: OECD, Main Economic Indicators—complete database. Main Economic Indicators. http://dx.doi.org/10.1787/data-00052-en. Copyright OECD. Reprinted with permission

Ouyang M (2011) On the cyclicality of R&D. Rev Econ Stat 93(2):542–553

Parisi ML, Schiantarelli F, Sembenelli A (2002) Productivity, innovation creation and absorption, and R&D: Micro evidence for Italy. Boston College Working Papers in Economics No 526. Available at SSRN: https://ssrn.com/abstract=302368 or http://dx.doi.org/102139/ssrn302368

Paunov C (2012) The global crisis and firms investments in innovation. Res Policy 41(1):24–35

Reifschneider D, Wascher W, Wilcox D (2015) Aggregate supply in the United States: recent developments and implications for the conduct of monetary policy. IMF Econ Rev 63(1):71–109

Romer PM (1990) Endogenous technological change. J Polit Econ 98(5, Part 2):S71–S102

Roodman D (2009) How to do xtabond2: an introduction to difference and system GMM in stata. Stata J 9(1):86–136(51). http://www.stata-journal.com/article.html?article=st0159

Salinger M, Summers LH (1983) Tax reform and corporate investment: a microeconometric simulation study. In: Feldstein M (ed) Behavioral simulation methods in tax policy analysis. University of Chicago Press, Chicago, pp 247–288

Whited TM (1992) Debt, liquidity constraints, and corporate investment: evidence from panel data. J Finance 47(4):1425–1460

Woerter M, Roper S (2010) Openness and innovation home and export demand effects on manufacturing innovation: panel data evidence for Ireland and Switzerland. Res Policy 39(1):155–164

Acknowledgements

I am grateful for helpful comments from Daniele Coen-Pirani, Marla Ripoll, Frederik-Paul Schlingemann, Sewon Hur, James Cassing, Kristle Romero-Cortés and seminar participants in the University of Pittsburgh. I also would like to thank the editor, Bertrand Candelon, and the anonymous reviewer for their constructive remarks on this version.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

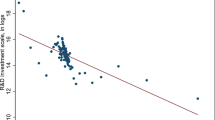

1.1 Construction of the data for Figs. 1, 2, and 3

-

Use the annual frequency data from the Compustat database for the years 1995–2015 and keep firms that have their headquarters located in the USA.

-

Keep firms that report a stock price and firms that have employment data. These steps improve consistency within the regression sample.

-

Keep firms that report positive R&D expenditure (XRD, data item #46) data. Convert the data into real values using the GDP deflator.Footnote 21

-

Classify firms with the following three-digit SIC codes as non-funded, high-tech firms: 283, 357, 366, 367, 382, 384 and 737.

-

Determine whether firms have access to bond markets using the existence of a bond rating by Standard and Poor’s.

-

Liquidity is defined as the ratio of cash and short-term investments as a fraction of total assets.

-

R&D-to asset ratio is defined as the ratio of R&D expenditures to total assets.

-

Winsorize variables at 1% from both tails.

-

Convert the data into quarterly units using linear interpolation.

1.2 Construction of the variables and regression samples

1.2.1 R&D stocks

The real R&D expenditures are calculated using the GDP deflatorFootnote 22 and R&D expenditure data from the Compustat database (XRD, data item #46). Real R&D capital stock is computed by a perpetual inventory method at the firm level by using the following equation:

where \(\mathrm{RD}_{i,t}\) represents the R&D stock; \(\mathrm{XRD}_{i,t}\) represents the real R&D expenditures of firm i at time t; and \(\delta \) is the depreciation rate. In order to obtain the initial R&D stock, the first observation of the real R&D expenditure is divided by a constant rate of depreciation (\(\delta \)) plus a growth rate (g).Footnote 23 Following Hall et al. (2005), I use 15% as the constant rate of depreciation.

The average growth rate of the R&D expenditure is calculated for each industry in the sample. For a firm that has the first R&D expenditure data at year t, g is the average growth rate of R&D expenditures in the industry that the firms belong to in the period between the first year the data are observed at the industry level and the year t. This procedure generates different growth rates for firms that belong to different industries. Also, I remove the firms that have their first observation of the R&D expenditures after 2006.

Before I apply the perpetual inventory method, I eliminate firms with zero or missing R&D expenditures for more than two consecutive years. The missing data points are obtained using linear interpolation. Firms that exit or have missing control variables between 2006Q4 and 2008Q4 are also eliminated. Since this sample is financially stronger, it might lead to underestimation of financing constraints. The sample only consists of firms that have their head quarters in the USA; therefore, the results cannot be generalized to other economies.

1.2.2 Capital stocks

Compustat reports the book value of capital (PPEGT, data item #7) and capital expenditures (CAPX, data item #145); however, for this analysis, the replacement value of capital stock is relevant. Following Salinger and Summers (1983), Fazzari et al. (1988) and Eberly et al. (2008), the replacement value of capital stock is computed by using the following recursion:

The initial value for \(K_i\) is set to the first observation in the PPEGT series for firm, i. \(P_{K,t}\) refers to the price of capital and is the implicit price deflator for nonresidential investment obtained from FRED.Footnote 24\(L_j\) refers to the useful life of capital goods in industry j. The useful life of capital goods is calculated as

\(\mathrm{DP}_{it}\) refers to the depreciation and amortization (Compustat Data Item #14) for firm i at year t. \(N_j\) refers to the number of firms in industry j.

1.2.3 Other variables

-

Tobin’s Q (Market-to-book ratio of firm’s assets) is defined following Brown and Petersen (2011):

$$\begin{aligned} Q=\frac{(\mathrm{CSHO}\cdot \mathrm{PRCCF})+ \mathrm{AT-CEQ}}{\mathrm{AT}_{-1}} \ , \end{aligned}$$where the first variable in the numerator is the market value of equity, which is equal to common shares outstanding (CSHO, data item # 25) times price close (PRCCF, data item #199). Then, total assets (AT, data item #120) net of common equity (CEQ, data item # 60) are added.

-

Sales growth is the log difference of net sales (SALE, data item #117) and denoted by \(\Delta \log (\mathrm{SALE})\).

-

Liquidity is denoted by LIQ and defined as cash and short-term investments (CHE, data item #1) divided by total assets (AT, data item #120).

Firm age is computed based on the year in which price close data (PRCCF) are first observed in the Compustat database. If the firm has data for less than 15 years after the first observation of PRCCF, it is listed as young; otherwise, it is considered mature. Firm size is computed based on its number of employees (EMP, data item #29). If the firm’s number of employees is below (above) the 75th percentile of the whole sample of firms, then it is listed as small (large).

1.2.4 R&D regression sample

This dataset is obtained from the Compustat database between the years 2006 and 2008 and is in quarterly frequency. I choose firms that are in the manufacturing sector and have no missing data on 2006Q4, 2007Q4 and 2008Q4. I keep firms that have their headquarters in the USA (based on Compustat variable, LOC). I remove firms that have gone through mergers and acquisitions during this period (i.e., for these firms, DSLRN is equal to one). Firms without any employment data, R&D stock data, or stock price data are also removed.

1.2.5 R&D, capital and inventory regression sample

I applied steps similar to those of the construction of the R&D sample. Besides the R&D stock, firms should also have capital stock, and real inventory data for 2006Q4, 2007Q4 and 2008Q4. The inventory data (INVT, data item # 3 ) are deflated using the CPI.Footnote 25

Rights and permissions

About this article

Cite this article

Kabukcuoglu, Z. The cyclical behavior of R&D investment during the Great Recession. Empir Econ 56, 301–323 (2019). https://doi.org/10.1007/s00181-017-1358-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-017-1358-7