Abstract

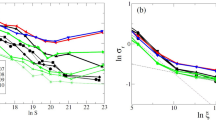

We introduce a new system of stochastic differential equations which models dependence of market beta and unsystematic risk upon size, measured by market capitalization. We fit our model using size deciles data from Kenneth French’s data library. This model is somewhat similar to generalized volatility-stabilized models. The novelty of our work is twofold. First, we take into account the difference between price and total returns (in other words, between market size and wealth processes). Second, we work with actual market data. We study the long-term properties of this system of equations, and reproduce observed linearity of the capital distribution curve. In the “Appendix”, we analyze size-based real-world index funds.

Similar content being viewed by others

References

Banner, A.D., Fernholz, D.: Short-term relative arbitrage in volatility-stabilized markets. Ann Finance 4(4), 445–454 (2008)

Banner, A.D., Fernholz, E.R., Karatzas, I.: Atlas models of equity markets. Ann Appl Probab 15(4), 2330–2996 (2005)

Banner, A.D., Fernholz, E.R., Ichiba, T., Karatzas, I., Papathanakos, V.: Hybrid Atlas models. Ann Appl Probab 21(2), 609–644 (2011)

Banz, R.W.: The relationship between return and market value of common stocks. J Financ Econ 9(1), 3–18 (1981)

Barnes, C., Sarantsev, A.: A note on jump Atlas models. Braz J Probab Stat 34(4), 844–857 (2020)

Chatterjee, S., Pal, S.: A phase transition behavior for Brownian motions interacting through their ranks. Probab Theory Rel Fields 147(1), 123–159 (2010)

Fama, E.F., French, K.R.: Common risk factors in the returns on stocks and bonds. J Financ Econ 33(1), 3–56 (1993)

Fama, E.F., French, K.R.: The capital asset pricing model: theory and evidence. J Econ Perspect 18(3), 25–46 (2004)

Fernholz, E.R.: Stochastic Portfolio Theory. Applications of Mathematics, vol. 48. New York: Springer (2002)

Fernholz, E.R., Karatzas, I.: Relative arbitrage in volatility-stabilized markets. Ann Finance 1(2), 149–177 (2005)

Fernholz, E.R., Karatzas, I.: Stochastic Portfolio Theory: An Overview. Mathematical Modeling and Numerical Methods in Finance, Handbook of Numerical Analysis, pp. 89–168 (2009)

Fernholz, E.R., Karatzas, I., Kardaras, C.: Diversity and relative arbitrage in equity markets. Finance Stoch 9(1), 1–27 (2005)

Jourdain, B., Reygner, J.: Capital distribution and portfolio performance in the mean-field Atlas model. Ann Finance 11(2), 151–198 (2015)

Karatzas, I., Sarantsev, A.: Diverse market models of competing Brownian particles with splits and mergers. Ann Appl Probab 26(3), 1329–1361 (2016)

Karatzas, I., Shreve, S.E.: Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics, vol. 113. New York: Springer (1998)

Meyn, S.P., Tweedie, R.L.: Stability of Markovian processes II: continuous-time processes and sampled chains. Adv Appl Probab 25(3), 487–517 (1993)

Meyn, S.P., Tweedie, R.L.: Stability of Markovian processes III: Foster–Lyapunov criteria for continuous-time processes. Adv Appl Probab 25(3), 518–548 (1993)

Pal, S.: Analysis of market weights under volatility-stabilized market models. Ann Appl Probab 21(3), 1180–1213 (2011)

Pal, S., Wong, T.-K.L.: The geometry of relative arbitrage. Math Financ Econ 10(3), 263–293 (2016)

Pickova, R.: Generalized volatility-stabilized processes. Ann Finance 10(1), 101–125 (2014)

Semenov, A.: The small-cap effect in the predictability of individual stock returns. Int Rev Econ Finance 38, 178–197 (2015)

Sharpe, W.F.: Capital asset prices: a theory of market equilibrium under conditions of risk. J Finance 19(3), 425–442 (1964)

Shkolnikov, M.: Competing particle systems evolving by interacting Lévy processes. Ann Appl Probab 21(5), 1911–1932 (2011)

Shkolnikov, M.: Large systems of diffusions interacting through their ranks. Stoch Process Appl 122(4), 1730–1747 (2012)

Shkolnikov, M.: Large volatility-stabilized markets. Stoch Process Appl 123(1), 212–228 (2013)

van Dijk, M.A.: Is size dead? A review of the size effect in equity returns. J Bank Finance 35(12), 3263–3274 (2011)

Zvonkin, A.K.: A transformation of the phase space of a diffusion process that will remove the drift. Math Sbornik 22(1), 129–149 (1974)

Acknowledgements

We thank the Department of Mathematics and Statistics at our University of Nevada, Reno, for welcoming and supportive atmosphere and for fostering research collaboration between faculty and students (undergraduate and graduate). We thank the referees for useful remarks and positive responses.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix: Statistical analysis of size-based index funds

Appendix: Statistical analysis of size-based index funds

These size deciles of the CRSP universe are not directly investable. But there exist size-based funds available for individual investors. Among many of them, let us take JKJ, JKG, JKD: iShares Morningstar Small-Cap, Mid-Cap, and Large-Cap exchange-traded funds. These are based on largest 70%, next 20%, and next 7% of the total universe of stocks. In other words, Large-Cap corresponds to Deciles 1–7 weighted by their market capitalizations, Mid-Cap corresponds to Deciles 8–9 weighted by their market capitalizations, and Small-Cap corresponds to the top 7% of the bottom Decile 10.

Monthly total arithmetic returns for these funds are taken from BlackRock web site, July 2004 – August 2020. For risk-free returns, we take 1-month Treasury Constant Maturity Rate from Federal Reserve Economic Data web site, observed at the last day of each month June 2004 – July 2020. We compute geometric versions of these returns. From each such rate r, we obtain geometric total monthly returns for the next month \(\ln (1 + r/1200)\). Then we compute equity premia \(P_S, P_M, P_L\) for these funds. Regress the first two upon the third:

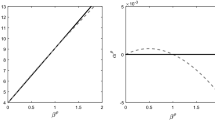

The quantile–quantile plots, Shapiro–Wilk and Jarque–Bera normality tests, and autocorrelation function plots allow us to assume that each series of residuals can be modeled by i.i.d. normal distribution. Thus we can apply standard Student tests for regression coefficients. The 95% confidence intervals for each of \(\alpha _S\) and \(\alpha _M\) contain zero. Thus we can assume that \(\alpha _S = \alpha _M = 0\), but the confidence intervals for \(\beta _S\) and \(\beta _M\) do not contain 1. Point estimates of these coefficients are: \(\beta _S = 1.27\), \(\beta _M = 1.15\). Estimates for standard errors for residuals, and cross-correlation between residuals are: \(\sigma _S = 0.026\), \(\sigma _M = 0.019\), \(\rho = 0.83\). The \(R^2\) values for each regression are 87% and 80%. Thus we see that the CAPM works for actual traded size-based funds.

Rights and permissions

About this article

Cite this article

Flores, B., Ofori-Atta, B. & Sarantsev, A. A stock market model based on CAPM and market size. Ann Finance 17, 405–424 (2021). https://doi.org/10.1007/s10436-021-00390-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10436-021-00390-8

Keywords

- Capital asset pricing model

- Stochastic differential equations

- Capital distribution curve

- Stochastic stability

- Market weight