Abstract

We determine the optimal life-cycle path of pension premiums during the working ages and pension benefits during retirement, assuming that households can choose these freely. We calibrate the model on Dutch data. The optimization takes into account the fact that incomes generally rise during the working ages and that children are generally present in young households. Both features lead to an upward sloping path of optimal pension premium rates over the working life, while under the current pension system this is rather flat. The welfare gains from implementing the optimal pension system depend on the specification of the model, but can be sizable. A potentially lower return on pension assets in the future implies a further delay of optimal pension premiums during the working ages and a lower optimal pension benefit after retirement. Differentiating the path of pension premiums and benefits according to the level of educational attainment of the main income earner brings only small additional welfare gains compared to the situation in which pension premium rates are based on the average income profile in the Dutch economy.

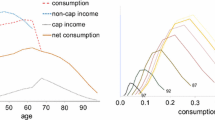

Similar content being viewed by others

Notes

For current participants in Individual Defined Contribution contracts, employers may opt for continuing the current age-dependent (and age-increasing) pension premium path (Ministry of Social Affairs and Employment 2020, p. 6).

Pension contribution rates show a significant rise with age only in Switzerland, see www.bsv.admin.ch/bsv/en/home/social-insurance/bv/grundlagen-und-gesetze/grundlagen/sinn-und-zweck.html.

For a three person household, for instance, the factor is smaller than 3. Section 3 elaborates on this.

For example social assistance, unemployment benefit, child related transfers.

For simplicity, average and marginal tax rates in both phases are set equal. This is further discussed in “Appendix 1.3”.

The average premium rate of the following five pension funds in 2020 in the Netherlands: ABP, PFZW, PBFbouw, PMT and Shell pension fund.

See for example the split used by the pension fund ABP: https://www.abp.nl/pensioen-bij-abp/pensioenpremie/.

In reality households can draw down her assets earlier. We make this assumption in order to facilitate the comparison with the family model. In the optimum of this model, the household draws down their assets after the age at which the pension benefit becomes available \(t_{aow}\), see Fig. 4c.

In the year 2010, the average labor market participation of men and women aged 50–55 years was 83% dropping to 73% for the age category of 55–60 years and to 39% for the age category of 60–65 years (Statistics Netherlands, CBS).

In the year 2018, the average labor market participation of men and women aged 50–55 years was 85% dropping to 79% for the age category of 55–60 years and to 62% for the age category of 60–65 years (Statistics Netherlands, CBS).

More information regarding how the equivalence factors are set can be found at: https://www.cbs.nl/nl-nl/achtergrond/2004/25/equivalentiefactoren-1995-2000.

https://www.abp.nl/english/investments/, section Investment Results. However, future rates of return are very uncertain.

The reference to the year 2010 is due to the fact that our income is transformed in real values using the CPI with a base in the year 2010.

In reality however average and marginal tax rates differ, both in size and in their impact. A high average tax rate reduces income and thus increases the marginal utility of consumption. As a result it increases the allocation of consumption to years in which the average tax rate is relatively high, reducing saving. A high marginal tax rate has the opposite effect. It reflects that a large part of pension savings goes untaxed and thus stimulates it in these years.

In the Netherlands around 70% of the pension premium is paid by the employer, and 30% by the employee, see for example the premium structure of ABP: https://www.abp.nl/pensioen-bij-abp/pensioenpremie/. Our modelling of the effects on net incomes and consumption nonetheless assumes that the full 100% is effectively paid by the employee. This is explained in the main text in Sect. 2.3.

References

Alan, S., & Browning, M. (2010). Estimating intertemporal allocation parameters using synthetic residual estimation. The Review of Economic Studies, 77(4), 1231–1261.

Attanasio, O. P., & Weber, G. (2010). Consumption and saving: Models of intertemporal allocation and their implications for public policy. Journal of Economic Literature, 48(3), 693–751.

Bick, A., & Choi, S. (2013). Revisiting the effect of household size on consumption over the life-cycle. Journal of Economic Dynamics and Control, 37(12), 2998–3011.

Crawford, R., O’Brien, L., & Sturrock, D. (2021). When should individuals save for retirement? Predictions from an economic model of household saving behaviour. Briefing note 326, IFS.

Crawford, R., & O’Dea, C. (2020). Household portfolios and financial preparedness for retirement. Quantitative Economics, 11(2), 637–670.

Cui, J. (2008). Dc pension plan defaults and individual welfare. Netspar discussion paper 09/2008-034.

de Kok, C. (2021). Finding an optimal age-dependent pension premium path for Dutch households, Erasmus University of Rotterdam.

Domeij, D., & Klein, P. (2013). Should day care be subsidized? Review of Economic Studies, 80(2), 568–595.

Elmendorf, D. W. (1996). The effect of interest-rate changes on household saving and consumption: A survey. Finance and economics discussion series 96-27, Board of Governors of the Federal Reserve System (US).

French, E. (2005). The effects of health, wealth, and wages on labour supply and retirement behaviour. Review of Economic Studies, 72(2), 395–427.

Fuchs-Schundeln, N. (2008). The response of household saving to the large shock of German reunification. American Economic Review, 98(5), 1798–1828.

Gomes, F., Michaelides, A., & Polkovnichenko, V. (2009). Optimal savings with taxable and tax-deferred accounts. Review of Economic Dynamics, 12(4), 718–735.

Gourinchas, P.-O., & Parker, J. A. (2002). Consumption over the life cycle. Econometrica, 70(1), 47–89.

Guvenen, F., & Smith, A. A. (2014). Inferring labor income risk and partial insurance from economic choices. Econometrica, 82, 2085–2129.

Havranek, T., Horvath, R., Irsova, Z., & Rusnak, M. (2015). Cross-country heterogeneity in intertemporal substitution. Journal of International Economics, 96(1), 100–118.

Laitner, J., & Silverman, D. (2012). Consumption, retirement and social security: Evaluating the efficiency of reform that encourages longer careers. Journal of Public Economics, 96(7–8), 615–634.

Ministry of Social Affairs and Employment. (2020). Hoofdlijnennotitie pensioenakkoord. Technical report, SZW.

Nishiyama, S., & Smetters, K. (2007). Does social security privatization produce efficiency gains? The Quarterly Journal of Economics, 122(4), 1677–1719.

Rabaté, S. & Rellstab, S. (2021). The child penalty in the Netherlands and its determinants. Discussion paper 424, Centraal Planbureau.

Scholz, J. K., Seshadri, A., & Khitatrakun, S. (2006). Are Americans saving “optimally" for retirement? Journal of Political Economy, 114(4), 607–643.

Scott, J., Shoven, J. B., Slavov, S. & Watson, J. G. (2021). Is automatic enrollment consistent with a life cycle model? Working paper 28396, National Bureau of Economic Research.

SER. (2019). Naar een nieuw pensioenstelsel. Ser-advies, Sociaal-Economische Raad.

Summers, L. H. (1984). The after tax rate of return affects private savings. American Economic Review, 74(2), 249–253.

Tweede Kamer. (2020). Memorie van Toelichting Wet Toekomst pensioenen. Technical report 6530, Tweede Kamer.

Van Tilburg, I., Kuijpers, S., Nibbelink, A. & Zwaneveld, P. (2019). Gamma: Een Langetermijnmodel voor de Houdbaarheid van de Overheidsfinanciën, CPB Achtergronddocument.

Vrouwerff, E. J. V. (2021). Marginale druk kan twistpunt worden aan formatietafel. Technical report 4797, Economische en Statistische Berichten.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

1.1 Summary Statistics

1.2 Optimal Pension Premium Rates with Progressive Income Tax Rates

In this appendix we check the robustness of the results to the assumption that income tax rates are flat. For simplicity, the baseline scenario makes the assumption of flat tax rates. This assumption may not be innocuous, because a progressive income tax rate will flatten the life-cycle profile of net household income. Consequently, the scope for age dependent pension premium rates declines.

Throughout the paper we use the policy variables (for example the value of the pension franchise and the pension cap) from the year 2010, the middle of the period for which the income data is available (2006–2013). However, in the case of the tax code, we choose to use the average tax rates corresponding to the year 2020. We make this choice because income tax rates have become substantially more progressive since 2010. The relationship between the gross income and the average tax rate we assume is similar to the one estimated in Vrouwerff (2021) (see Fig. 14, left panel). Because information about the average tax rates after the AOW age is missing in Vrouwerff (2021), the income tax is kept flat at 22%, the same as in the baseline scenario. The average tax rates corresponding to the life-cycle income profile of the average Dutch household are shown in Fig. 14, right panel.

Progressive average income tax rates

Using the progressive tax rate depicted in Fig. 14, we compute the optimal consumption and savings schedule. The results are presented in Fig. 15. Comparing these with the results from the baseline scenario (Fig. 4), we see that the life-cycle profile of the savings rates is slightly less upward sloping. Wealth accumulation and pension benefits are also smaller in the case of both the earner and the family model. The differences are however small. The welfare gains from implementing the optimal pension system decline to 2.5% from 3.1% in the case of the family model and 1.3% from 2.6% in the case of the earner model. If we impose borrowing constraints, welfare gains drop to 2.4% and 1%, respectively.

The current pension system (solid line), the family model (dashed line) and earner model (circles): optimal wealth, consumption, savings ratio and pension benefits

1.3 Derivation of the Optimization Problem

Appendix 1.3 contains a step by step derivation of the equations presented in the paper. We start directly with the family model and mention what changes must be implemented in the derivations in order to obtain the earner model.

The household chooses each period how much to consume (\(c_t\)) and implicitly how much wealth to accumulate (\(a_t\)) by maximizing the present value of the utility of standardized consumption:

where \(\beta\) is the time preference parameter, \(\psi _t\) is the probability to survive until time t, \(n_t\) is the number of members in a household, \(\sigma\) is the inverse of the elasticity of intertemporal subsitution and \(eq_t\) equals the equivalence factor at time t. In the earner model, the number of household members (\(n_t\)) is equal to 2 at every age because the consumption of children is not valued in the utility function. Consequently, this variable drops from the subsequent equations.

The decision of the household is subject at each age t to a budget constraint:

where \(y_t\) is the income of the household comprised of labor income until the age when the pay-as-you-go benefit is received (\(t_{aow}\)) and the pay-as-you-go pension benefit (AOW) afterwards, R is the rate of return, \(a_t\) is the wealth, the per capital transfers \(tr_t\) come from the fact that a fraction of the population alive at time \(t-1\) dies and the bequests are divided between the members still alive at time t.

The size of the bequests left by the people who die is given by:

where \(R a_{t-1}\) is the per capita wealth accumulated by people alive at time \(t-1\), \(l_{t-1}\) is the number of people alive at time \(t-1\), \(\frac{\psi _t}{\psi _{t-1}}\) is the probability to survive between period \(t-1\) and t and \(\Big ( 1- \frac{\psi _t}{\psi _{t-1}} \Big )\) is the probability to die between period \(t-1\) and t. We divide total bequests among the people that are still alive at time t:

Next we take into account that the ratio of people alive at time t and people alive at time \(t-1\) is equal to the probability to survive between periods \(t-1\) and t:

We substitute relation 26 into 25 and obtain the per capita transfer coming from bequests:

Finally, we substitute 28 in the period by period per capita budget constraint from relation 23 and obtain:

We use the individual budget constraints to obtain the lifetime budget constraint:

The consumption can be described by:

where \(p_t\) equals the amount of pension money (either being saved or dis-saved) and \(\omega _t\) equals the percentage of tax on income net of pension premiums paid at age t: 36% until the age of 65 and 22% afterwards. For simplicity, average and marginal tax rates in both phases are set equal.Footnote 17 The tax paid is equal to \(tax_t = (y_t-p_t)\omega _t\), so expenditures (consumption and tax) can be rewritten asFootnote 18:

Therefore, Eq. 30 can be rewritten as:

The problem that the household solves becomes:

The first order conditions of the above maximization problem are:

It follows that the relationship between first period consumption (\(c_1\)) and the consumption in period t (\(c_t\)) is given by:

Next, we substitute Eq. 36 in the life-time budget constraint of the household from Eq. 33:

Now we can derive a closed-form solution for the first period consumption of the household:

Rights and permissions

About this article

Cite this article

Ciurilă, N., de Kok, C., Rele, H.t. et al. Optimizing the Life-Cycle Path of Pension Premium Payments and the Pension Ambition in the Netherlands. De Economist 170, 69–105 (2022). https://doi.org/10.1007/s10645-022-09400-0

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10645-022-09400-0