Abstract

Corporate income taxation, by affecting the after-tax cost of funding, has implications for a bank’s incentive to securitize. Using a sample of OECD banks over the period 1999–2006, we find that corporate income taxation led to more securitization at banks that are constrained in funding markets, while it did not affect securitization at unconstrained banks. This is consistent with prior theories suggesting that the tax effects of securitization depend on the extent to which banks face funding constraints. Our results suggest that current corporate income tax systems have distorting effects on banks’ securitization decisions.

Similar content being viewed by others

Notes

Decreased incentives for monitoring and excessive securitization contributed to the increase of systemic risk and eventually the subprime crisis. Nijskens and Wagner (2011) find evidence that banks issuing credit default swaps (CDSs) and collateralized loan obligations (CLOs) pose greater systemic risk.

For example, even though the Indian securitization market grew 15 % in the fiscal year 2012, a pending amendment which made the tax status of pass-through entities uncertain hit the market. “Due to lack of clarity on tax incidence on pass-through vehicles, the securitization business has come to a virtual standstill,” said Vimal Bhandari, CEO of Indostar Capital Finance. See “Tax issue hits securitization market hard” in Indian Express.

In this paper, the definition of securitization is restricted to the off-balance sheet activity of issuing ABS. This definition is much narrower than the general concept which includes selling loans, issuing standby letters of credit and loan commitments.

Despite a general declining trend, corporate income tax rates remain substantially different across countries. For instance, Ireland and Turkey have effective marginal CIT rates below 10 %, whereas Germany and Japan have rates above 35 %.

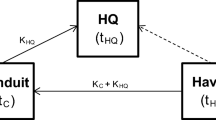

In practice, tax neutrality is usually accomplished in a variety of ways. First, offshore SPVs are widely used to maintain no taxable presence in originator’s jurisdiction. Set up in tax havens or tax-friendly countries to OECD, such as Cayman Islands, Irish docks and Jersey, SPVs have access to tax avoidance strategies unpermitted at home jurisdictions. Second, SPVs are structured as tax transparent pass-through entities. For instance, treated as tax transparent and pass-through, real estate mortgage investment conduits (REMICs) are generally not taxed in the U.S. Third, SPVs can be designed to have little material income tax liability, i.e., its deductible expenses perfectly offset income, reducing taxable income to zero.

Certain contract features, such as offering implicit recourse, holding equity tranche and over-collateralization, are designed to alleviate the moral hazard problem and to reduce the agency cost of securitization. Consistent with theoretical predictions of reduced incentives to carefully screen and monitor borrowers, some empirical studies find a decline in the credit quality in securitized loans (Keys et al. 2010; Purnanandam 2011; Keys et al. 2012).

Fixed costs usually include the costs associated with setting up SPVs, rating fees, auditing and legal expenses.

Gilje et al. (2013) find that banks experiencing deposits windfalls in U.S. shale-boom counties tend to fund their mortgage lending through low cost deposits instead of securitization.

For instance, the Italian market of securitization had not started growing remarkably until the enactment of Law 130 in 1999.

In practice, small banks with no direct access to ABS markets might sell loans to large institutions that pool and securitize them. This means in some cases the underlying assets of ABS are not originated by the sponsor of ABS, which may bring noises and biases to our analysis. Fortunately, this usually happens in the deals in which large investment banks act as sponsors and are excluded from our sample. Therefore, most securitizing banks in our sample originate loans as the underlying assets and complete off-balance sheet securitization themselves.

Using bank names and countries of residence as a reference, Panetta and Pozzolo (2010) match originators of securitization in Dealogic with banks in Bankscope in a similar study of motivations for bank securitization. They end up with a sample of 696 matched pairs. It is worth noting that their research covers a longer period (1991–2007), more countries (140 countries) and various types of securitization (asset-backed securities (ABSs), mortgage-backed securities (MBSs), collateralized loan obligations (CLOs) and collateralized debt obligations (CDOs)), therefore they have more matched securitizing banks.

We thank the referee for clarifying this point.

Due to data limitation, we have little traceable information of SPVs in most securitization transactions. However, this argument is in line with anecdotal facts that SPVs do have an advantage as long as they are, indeed, truly bankruptcy remote and off balance sheet.

We do not include the bank size into regressions since we have already considered the crucial effect of bank size on securitization and restricted our sample to large banks only.

It is less likely that leverage leads to endogeneity bias in our analysis. First, in the model of Han et al. (2014) in the absence of securitization market, bank leverages are determined by loan and deposit market conditions as well as corporate tax rates. In the securitization decision, it is the trade-off of marginal costs of on and off-balance sheet financing, rather than bank leverage, that determines whether to securitize or not. Therefore, once we include tax rates, the funding constraint dummy, and the interaction of the two, it is unlikely our results are contaminated by omitted variable bias. We also control for other bank level variables, regulatory variables and macroeconomic variables to mitigate the concern of omitted variable bias. Second, securitization may affect bank leverage ex post as loans are removed from balance sheets and bank excess capital decreases. By contrast, in the model of Han et al. (2014) there is no channel through which leverages directly affect securitization. Therefore, we are less worried about reverse causality. In addition, we explicitly include bank leverages (Equity/TA) in our specifications to control for other possible channels through which leverages may directly or indirectly affect securitization, for instance regulatory capital arbitrage. Third, the average standard deviation of equity over total assets for each bank in our sample period is 1.09, indicating time-varying leverage. Therefore, the assumption of persistent leverage does not hold and hence endogeneity bias is less of concern. We are grateful to the referee for raising this point.

Securitizing banks are defined as banks that issues asset-backed securities.

The small sample means of SAR and S A R a d j are primarily driven by the large group of nonsecuritizing banks (4158 banks or 94 % of our sample). The means of SAR and S A R a d j are 7.7 % and 5.9 % for the group of securitizing banks, which are reasonable.

We thank the referee for suggesting this alternative dependent variable.

References

Affinito M, Tagliaferri E (2010) Why do (or did) banks securitize their loans? Evidence from Italy. J Financ Stability 6:189–202

Albertazzi U, Gambacorta L (2010) Bank profitability and taxation. J Bank Finance 34:2801–2810

Ambrose B, LaCour-Little M, Sanders A (2005) Does regulatory capital arbitrage, reputation, or asymmetric information drive securitization? J Financ Serv Res 28:113–133

Bank for International Settlements (2011) Report on asset securitisation incentives. Basel Committee on Banking Supervision. Basel, Switzerland

Bannier C, Hänsel D (2008) Determinants of European banks’ engagement in loan securitization. Deutsche Bundersbank, mimeo

Barth J, Caprio G, Levine R (2001) The regulation and supervision of banks around the world: A new database. World Bank, mimeo

Calomiris C, Mason J (2004) Credit card securitization and regulatory arbitrage. J Financ Serv Res 26:5–27

Cardone-Reportella C, Samaniego-Medina R, Trujillo-Ponce A (2010) What drives bank securitization? The Spanish experience. J Bank Finance 34:2639–2651

Carlstrom C, Samolyk K (1995) Loan sales as a response to market-based capital requirements. J Bank Finance 19:627–646

Demirgüç-Kunt A, Huizinga H (1999) Determinants of commercial bank interest margins and profitability: some international evidence. World Bank Econ Rev 13(2):379–408

Demirgüç-Kunt A, Huizinga H (2001) The taxation of domestic and foreign banking. J Public Econ 79:429–453

Demsetz R (2000) Bank loan sales: a new look at the motivations for secondary market activity. J Financ Res 23:192–222

Gilje E, Loutskina E, Strahan P (2013) Exporting liquidity: branch banking and financial integration. University of Virginia Working Paper

Gorton G, Pennacchi G (1995) Banks and loan sales: Marketing nonmarketable assets. J Monet Econ 35:389–411

Gorton G, Souleles N (2007) Special purpose vehicles and securitization, 4th edn. University of Chicago Press, Chicago

Greenbaum S, Thakor A (1987) Bank funding modes: securitization versus deposits. J Bank Finance 111:379–401

Han J, Park K, Pennacchi G (2014) Corporate taxes and securitization. J Finance. forthcoming

Huizinga H (2004) The taxation of banking in an integrating Europe. Int Tax Public Finance 61:551–586

Huizinga H, Voget J, Wagner W (2014) International taxation and cross-border banking. Am Econ J Econ Policy. forthcoming

International Monetary Fund (2010) A fair and substantial contribution by the financial sector: Final report for the G-20. International Monetary Fund. Washington, D.C

Keen M (2011) Rethinking the taxation of the financial sector. CESifo Econ Stud 57:1–24

Keys B, Mukherjee T, Seru A, Vig V (2010) Did securitization lead to lax screening? Evidence from subprime loans. Quart J Econ 125(1):307–362

Keys B, Seru A, Vig V (2012) Lender screening and the role of securitization: evidence from prime and subprime mortgage markets. Rev Financ Stud 25(7):2071–2108

Laeven L, Levine R (2009) Bank governance, regulation and risk taking. J Financ Econ 93(2):259–275

Loutskina E (2011) The role of securitization in bank liquidity and funding management. J Financ Econ 100:663–684

Loutskina E, Strahan P (2009) Securitization and the declining impact of bank finance on loan supply: evidence from mortgage originations. J Finance 64(2):861–889

Nijskens R, Wagner W (2011) Credit risk transfer activities and systemic risk: how banks became less risky individually but posed greater risks to the financial system at the same time. J Bank Finance 35:1391–1398

Panetta F, Pozzolo A (2010) Why do banks securitize their assets? Bank-level evidence from over one hundred countries. Banca d’Italia, mimeo

Pavel C, Phillis D (1987) Why commercial banks sell loans? An empirical analysis. Fed Reserve Bank Chicago Proceedings, July/August: 145–165

Pennacchi G (1988) Loan sales and the cost of bank capital. J Finance 43:375–395

Purnanandam A (2011) Originate-to-distribute model and the subprime mortgage crisis. Rev Financ Stud 24(6):1881–1915

Shaviro D (2009) The 2008 financial crisis: implications for income tax reform. New York University Working Paper

Acknowledgments

We are indebted to George Pennacchi and Wolf Wagner for the inspiring discussions. We thank an anonymous referee, Steve Bond, Michael Devereux, Bálint Horváth (discussant), Kebin Ma, José-Luis Peydró and Jing Xing (discussant) for their insightful comments. We too are grateful to participants at the GSS seminar at Tilburg university, 6th International Risk Management Conference, Banking summer school at Barcelona GSE, CBT doctoral meeting 2013 at Oxford University, University of Birmingham, University College London, and 13th FDIC-JFSR Annual Bank Research Conference for their comments. The usual disclaimer applies.

Author information

Authors and Affiliations

Corresponding author

Additional information

Jenny E. Ligthart suddenly passed away on November 21, 2012. She was always enthusiastic and tirelessly available to her students, anytime and anywhere. We remember her as an excellent researcher, a professional teacher, a helpful supervisor and a close friend.

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Gong, D., Hu, S. & Ligthart, J.E. Does Corporate Income Taxation Affect Securitization? Evidence from OECD Banks. J Financ Serv Res 48, 193–213 (2015). https://doi.org/10.1007/s10693-014-0210-x

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10693-014-0210-x