Abstract

The combinatorial clock auction is a two-stage auction format, which has been used to sell spectrum licenses worldwide in the recent years. It draws on a number of elegant ideas inspired by economic theory. A revealed preference activity rule should provide incentives to bid straightforward, i.e., consistent with the bidders’ valuations on a payoff-maximizing package, in each round of the clock phase. A second-price rule should set incentives to bid truthfully in both phases. If bidders respond to these incentives and bid straightforward in the clock phase and truthful in the second sealed-bid stage, then the auction is fully efficient. Unfortunately, bidders might neither bid straightforward in the clock phase nor truthful on all packages in the second sealed-bid stage due to strategic reasons or practical limitations. We introduce metrics based on Afriat’s Efficiency Index to analyze straightforward bidding and report on empirical data from the lab and from the field in the British 4G auction in 2013 and the Canadian 700 MHz auction in 2014, where the bids were made public. The data provides evidence that bidders deviate significantly from straightforward bidding in the clock phase, which can restrict the bids they can submit in the supplementary phase. We show that such restrictions can have a significant negative impact on efficiency and revenue.

Similar content being viewed by others

Notes

The auction rules of the Canadian 700 MHz auction in 2014 can be found at http://www.ic.gc.ca/eic/site/smt-gst.nsf/eng/sf10583.html. The auction rules of the British auction in 2013 can be found at http://stakeholders.ofcom.org.uk/spectrum/spectrum-awards/awards-archive/completed-awards/800mhz-2.6ghz/.

Ausubel (2006) showed that there is an ascending auction with multiple price trajectories and item-level prices, which is efficient and yields the VCG allocation and payments. The auction runs one ascending auction with all bidders, and one with each bidder excluded in turn. However, this auction format is quite different from the clock auctions used in the field so far.

If \(x_t R_D x_s\) then it must not be the case that \(x_s P_D x_t\) for WARP to be satisfied.

If \(x_t R x_s\) then it must not be the case that \(x_s R x_t\) for SARP to be satisfied.

If \(x_t R x_s\) then it must not be the case that \(x_s P x_t\) for GARP to be satisfied.

\(x_i R_D x_j\) for any pair \((i,j)\) as all valuations are equal.

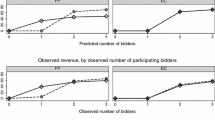

Let’s introduce a simple example to better illustrate how straightforward bidding can lead to inefficiency in the clock auction: Consider a market with two items \(\{A,B\}\) and three bidders. Bidder 1 has a value of $10 for \(A\), bidder 2 has a value of $4 for \(B\) and $10 for \(\{A,B\}\), and bidder 3 only has a value of $10 for the package \(\{A,B\}\). If all bidders bid straightforward starting with prices of zero and unit increments, then bidder 2 will never reveal his valuation for A, leading to 71% efficiency. Bidders 2 and 3 would actually drop out at a price of $5 for both items in the clock stage, which is when bidder 1 still bids on item \(A\). It is easy to extend the example and achieve very low revenue.

Since EE is the largest mobile service provider in the UK (Ofcom 2011), it might be surprising to describe them as secondary bidders. However, the classification was solely made based on the bids in this particular auction.

References

Afriat SN (1967) The construction of utility functions from expenditure data. Int Econ Rev 8(1):67–77

Afriat SN (1973) On a system of inequalities in demand analysis: an extension of the classical method. Int Econ Rev 14(2):460–472

Airiau S, Sen S (2003) Strategic bidding for multiple units in simultaneous and sequential auctions. Group Decis Negot 12(5):397–413. doi:10.1023/B:GRUP.0000003741.29640.ac

Arthur C (2013) 4G auction to be investigated by audit office after poor return. http://www.theguardian.com/technology/2013/apr/14/4g-auction-national-audit-office

Ausubel L, Baranov O (2014) Market design and the evolution of the combinatorial clock auction. Am Econ Rev Pap Proc 104(5):446–451

Ausubel LM (2006) An efficient dynamic auction for heterogeneous commodities. Am Econ Rev 96(3):602–629

Ausubel LM, Milgrom PR (2002) Ascending auctions with package bidding. Front. Theor. Econ. 1(1):1–42. http://www.ausubel.com/auction-papers/ascending-proxy-auctions.pdf

Ausubel LM, Cramton P, Milgrom P (2006) The clock–proxy auction: a practical combinatorial auction design. In: Cramton P, Shoham Y, Steinberg R (eds) Combinatorial auctions, chap 5. MIT Press, Cambridge, pp 115–138. The ISBN-10 is 0262514133

Bellantuono N, Ettorre D, Kersten G, Pontrandolfo P (2013) Multi-attribute auction and negotiation for e-procurement of logistics. Group Decis Negot 1–21. doi:10.1007/s10726-013-9353-7

Bichler M, Shabalin P, Wolf J (2011) Efficiency, auctioneer revenue, and bidding behavior in the combinatorial clock auction. In: Second conference on auctions. Market mechanisms and their applications (AMMA), New York, NY, USA

Bichler M, Shabalin P, Wolf J (2013a) Do core-selecting combinatorial clock auctions always lead to high efficiency? An experimental analysis of spectrum auction designs. Exp Econ 16:511–545

Bichler M, Shabalin P, Ziegler G (2013b) Efficiency with linear prices? A theoretical and experimental analysis of the combinatorial clock auction. In: INFORMS information systems research, pp 394–417

Bichler M, Goeree J, Mayer S, Shabalin P (2014) Spectrum auction design: simple auctions for complex sales. Telecommun Policy 38(7):613–622

Bundesnetzagentur (2010) Frequency Award 2010. http://www.bundesnetzagentur.de/cln_1931/EN/Areas/Telecommunications/Companies/FrequencyManagement/ElectronicCommunicationsServices/FrequencyAward2010_Basepage.html

Cramton P (2008) A review of the L-band auction. Technical report August. http://works.bepress.com/cramton/11/

Danish Business Authority (2012) Information memorandum—800 MHz auction. http://erhvervsstyrelsen.dk/file/251159/information-memorandum-800mhz-auction.pdf

Day RW, Cramton P (2012) Quadratic core-selecting payment rules for combinatorial auctions. Oper Res 60(3):588–603

Goeree JK, Lien Y (2013) On the impossibility of core-selecting auctions. Theor Econ (forthcoming). http://econtheory.org/

Gul F, Stacchetti E (1999) Walrasian equilibrium with gross substitutes. J Econ Theory 87(1):95–124

Janssen M, Karamychev V (2013) Gaming in combinatorial clock auctions. Technical report, Tinbergen Institute

Jewitt I, Li Z (2008) Report on the 2008 UK 10–40 GHz spectrum auction. Technical report. http://stakeholders.ofcom.org.uk/binaries/spectrum/spectrum-awards/completed-awards/jewitt.pdf

Knapek S, Wambach A (2012) Strategic complexities in the combinatorial clock auction. CESifo Working Paper Series 3983, CESifo Group Munich. http://ideas.repec.org/p/ces/ceswps/_3983.html

Lehmann D, Müller R, Sandholm T (2006) The winner determination problem. In: Cramton P, Shoham Y, Steinberg R (eds) Combinatorial auctions. MIT Press, chap 12. http://www.cs.cmu.edu/~sandholm/winner-determination-final.pdf

Levin J, Skrzypacz A (2014) Are dynamic vickrey auctions practical? Properties of the combinatorial clock auction. Stanford University working paper September

Milgrom P (2000) Putting auction theory to work: the simultaneous ascending auction. doi:10.1086/262118

Milgrom P (2004) Putting auction theory to work. Cambridge University Press, Cambridge

Milgrom PR, Weber RJ (1982) A theory of auctions and competitive bidding. Econometrica 50(5):1089–1122

Ofcom (2011) Everything Everywhere becomes the UKs largest network in terms of revenue. http://stakeholders.ofcom.org.uk/market-data-research/market-data/communications-market-reports/cmr11/telecoms-networks/5.48

Ofcom (2012) The wireless telegraphy (licence award) regulations 2012. http://www.legislation.gov.uk/uksi/2012/2817/contents/made

Ofcom (2013a) 800 MHz & 2.6 GHz auction data. http://stakeholders.ofcom.org.uk/spectrum/spectrum-awards/awards-archive/completed-awards/800mhz-2.6ghz/auction-data/

Ofcom (2013b) 800 MHz & 2.6 GHz combined award. http://stakeholders.ofcom.org.uk/spectrum/spectrum-awards/awards-archive/completed-awards/800mhz-2.6ghz/

Rothkopf MH (2007) Thirteen reasons why the vickrey-clarke-groves process is not practical. Oper Res 55(2):191–197

RTR (2013) Multiband Auction 800/900/1800 MHz. Rundfunk und Telekom Regulierungs-GmbH. https://www.rtr.at/en/tk/multibandauktion

Samuelson PA (1938) A note on the pure theory of consumer’s behaviour. Economica 5(17):61–71. http://www.jstor.org/stable/10.2307/2548836

Sano R (2012) Non-bidding equilibrium in an ascending core-selecting auction. Games Econ Behav 74:637–650

Scheffel T, Ziegler A, Bichler M (2012) On the impact of package selection in combinatorial auctions: an experimental study in the context of spectrum auction design. Exp Econ 15:667–692

Shapiro R, Holtz-Eakin D, Bazelon C (2013) The economic implications of restricting spectrum purchases in the incentive auctions. Georgetown University Washington working paper

Smeulders B, Spieksma FCR, Cherchye L, De Rock B (2012) Goodness of fit measures for revealed preference tests: complexity results and algorithms. aghedupl V(212):1–16. http://home.agh.edu.pl/~faliszew/COMSOC-2012/proceedings/paper_11.pdf

Smith C (2013) Did Ofcom’s 4G auction rules cost the UK an extra 3 billion? http://www.techradar.com/news/phone-and-communications/did-ofcom-s-4g-auction-rules-cost-the-uk-an-extra-3-billion-1138302

Varian HR (1990) Goodness-of-fit in optimizing models. J Econom 46:125–140. http://www.sciencedirect.com/science/article/pii/030440769090051T

Varian HR (2006) Revealed preference. In: Szenberg M, Ramrattan L, Gottesman AA (eds) Samuelsonian economics and the twenty-first century, January 2005, chap 6. Oxford University Press, Oxford, pp 99–115

Author information

Authors and Affiliations

Corresponding author

Appendix: Details on the Value Model and the Simulations based on the British 4G Auction

Appendix: Details on the Value Model and the Simulations based on the British 4G Auction

The value model used in our simulations in Sect. 6 is based on the British 4G auction in 2013 in which the 800 MHz as well as the 2.6 GHz band were sold (Ofcom 2013b). We will provide a brief description of the British auction and how we derived the value model for each bidder in our simulations, mirroring the main characteristics of this market. The valuations can be made available upon request.

1.1 Licenses Up for Sale

Table 6 illustrates the lots used in the auction. We simplified this band plan to allow for an easier analysis. The 800 MHz spectrum was split into two generic lots A(i) and A(ii) where A(ii) has twice as much bandwidth and eligibility points. Furthermore, the winner of A(ii) is obliged to use his spectrum to build a nationwide network. For simplicity, we neglected these legal details in our experiments and combined A(i) and A(ii) into one generic lot A with 6 licenses and the specifications of A(i).

The paired 2.6 GHz spectrum was split into three generic lots C, D(i), and D(ii) with amounts dependent on the bids submitted in the auction. D(i) and D(ii) are shared low power lots of different bandwidth whose winners will jointly use the same frequencies. The British auction rules allowed three different outcomes: First, up to 10 units of D(ii) are sold along with 10 units of C; second, up to 10 units of D(i) are sold along with 12 units of C, or third, the entire paired 2.6 GHz spectrum is sold in 14 units of C. Whichever allocation maximizes revenues wins. Based on the fact that 14 units of C were sold in the British auction and almost no bids containing shared low power lots were submitted, we discarded D(i) and D(ii) in our numerical experiments, as they did not seem to be important for this market.

For the unpaired 2.6 GHz spectrum (band E), only one lot with 9 units was used. However, the number of licenses that can actually be used is lower and dependent on the number of winners since one reserved block per winning package is required as a protection ratio between any two different users. In our simulations, we ignored this limitation and assumed 9 fully useable blocks as C is the least important band in the auction. The resulting list of bands used in our simulations can be found in Table 7.

In addition, a number of spectrum caps were imposed, some of which were also based on existing spectrum holdings in the British auction. For simplicity, we only used one simple spectrum cap that limits the amount of 800 MHz spectrum assigned to a single bidder to no more than 4 blocks or \(2\times 20\) MHz which is common in similar auctions.Footnote 8

1.2 Bidders in the British 4G Auction

Seven bidders participated in the auction and five of them won at least one license. As expected, the most valuable target—a pair of A blocks for building a nationwide network with maximum reach—was won by the two big incumbents Vodafone and Telefonica. Table 8 shows the results of the British auction using the simplified lots introduced in the previous section.

Since all auction data has been made publicly available, the segmentation of participants into four generic bidder types is based not only on the results, but also on actual bidding behavior throughout the auction. As illustrated in Fig. 7, there are four bidders who competed in all three bands: the primary bidders Vodafone and Telefonica as well as the secondary bidders Everything Everywhere and Hutchison 3G. The reason for separating them into two groups is the obvious strength of the primary bidders with regard to lot A. For these lots, the primary bidders’ bids were much higher than the final clock prices in the supplementary round, compared to both secondary bidders.Footnote 9 The 2.6 GHz Bidder Niche Spectrum Ventures was focused on the 2.6 GHz lots only while the small bidders MLL Telecom and HKT Company only competed for the licenses in the C band.

Visualization of bidding behavior throughout the clock rounds of the British 4G auction with a simplified band plan (\(\hbox {A}=red\), \(\hbox {B}=apricot\), \(\hbox {C}=blue\)). a Vodafone. b Telefonica. c Everything everywhere. d Hutchison 3G. e Niche spectrum ventures. f MLL Telecom. g HKT company. (Color figure online)

1.3 A Value Model for the Simulations

Based on the public bid data, we derived a value model, i.e., valuations for each bidder, which allowed us to run simulations and estimate the impact of different bidding strategies in Sect. 6. First, we defined individual base valuations for each bidder indicating how much he is willing to pay for a single license in a band. Second, intra-band synergies were defined for any package with more than one license within the same band up to a certain limit (e.g., 2 blocks of A, 4 blocks of B or C). More licenses of the same band exhibit decreasing marginal value beyond these limits. For the expensive A blocks we even assumed that no bidder is interested in winning more than two licenses. Third, inter-band synergies were defined increasing the value of a bundle comprising licenses from bands A and B. The mean base valuations were defined based on the final clock prices and the supplementary bids and can be found in Table 9. The primary bidders had a much higher valuation in the A band compared to other bidders, while we assumed similar valuations for the B and C bands. Even though the true valuations of bidders are unknown, this allowed for a reasonable sensitivity analysis in Sect. 6.

Based on the mean base valuations \(v\) in Table 9 the valuations for each simulation were determined based on two parameters, the relative strength of a bidder \(s_i\) and a random influence \(r_i\). Both values are drawn from a uniform distribution in the interval \([v\times 0.75, v\times 1.25]\) and multiplied with the mean base valuations \(v\) for each band. For example, consider a primary bidder with relative strength 0.8 and random influence for blocks A and B of 1.1 and 1.0, resp. His valuations are \(v_i(A) = 0.8 \cdot 1.1 \cdot \pounds 300\,\text {mn} = \pounds 264\,\text {mn}\) and \(v_i(B) = 0.8 \cdot 1.0 \cdot \pounds 70\,\text {mn} = \pounds 56\,\text {mn}\). Then we determined the valuation \(v_i(nX)\) for different bundles with \(n\) licenses within a band \(X\).

The first and second summand correspond to the linear increase in value when adding more blocks and the synergies on top of that. Both only increase in value until a threshold is reached. The third summand is only relevant when additional blocks are added, but with decreasing marginal value. The final valuation for a bundle within a band is computed as the sum of the licenses within a band multiplied by \((1+syn_i)\). All intra-band synergies \(syn_i(A)\) are drawn from a uniform distribution \([1.75;2.25]\). Only the synergies for the primary bidders in the A band were higher and drawn from a uniform distribution in the interval \([3.75;4.25]\) assuming that two blocks in A was their primary target. Figure 8 illustrates the resulting valuation function which is only valid for A for up to 2 blocks.

Plot of intra-band valuations

Finally, a uniformly distributed parameter is drawn for each bidder to determine his inter-band synergies for bands A and B. Synergies across these bands can be assumed to be much lower than intra-band synergies, and we use a uniform distribution in the interval \([0.0;0.2]\). The valuation for a bundle containing licenses from bands A and B is now computed as the sum of the valuations for inter-band bundles multiplied with \((1+syn_i)\). For example, a bidder’s valuation for a bundle \(ABBC\) comprised of one block of A, two blocks of B, and one license in band C is \(v_i(ABBC)=(v_i(A)+v_i(2B)+v_i(C))\cdot (1+syn_i)\). Based on the random variables above, we generated 10 different instances of the value model.

The correlation between the supplementary bids in the British 4G auction and the valuations generated with the above model is 0.957, indicating that the generated valuations are a reasonable basis for our simulation study.

Rights and permissions

About this article

Cite this article

Kroemer, C., Bichler, M. & Goetzendorff, A. (Un)expected Bidder Behavior in Spectrum Auctions: About Inconsistent Bidding and Its Impact on Efficiency in the Combinatorial Clock Auction. Group Decis Negot 25, 31–63 (2016). https://doi.org/10.1007/s10726-015-9431-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10726-015-9431-0