Abstract

Tax competition for capital has led to a trend where many countries levy lower taxes on interest income, often introducing differential taxation between interest and business income. This study analyzes the effect on firm debt usage. We exploit Germany’s 2009 tax reform, which introduced a final withholding tax on interest income with a flat rate 18 percentage points below the unchanged tax rate on income from unincorporated businesses, as a quasi-experiment. The results, based on firm-level panel data, indicate that firms increase their leverage when the tax rate on interest income decreases, albeit to a small degree.

Similar content being viewed by others

Notes

Similarly, Spain introduced a flat tax of 18 % on interest income from instruments with a maturity of less than 1 year in 2007, and France implemented an optional flat tax on interest income with a rate of 18 % in 2008. Other countries with this type of capital income taxes include Austria, the Czech Republic and Portugal (OECD 2013). Note that a DIT can also be implemented as a withholding tax; the distinction here depends on the treatment of normal returns to unincorporated business capital.

For the purpose of this article, we define business income as income from an unincorporated business and equity income as the broader category of income which in addition includes dividends from shares in corporations. Effectively, all equity income is taxed at a significantly higher rate than interest income. The tax on dividend income cumulates to a high rate that is similar to the tax rate on business income from unincorporated firms, because the corporate tax and the local business tax are not credited against the final withholding tax (see Sect. 2.1.).

For this international comparison, we consider equity investments in corporations, because of the more important role of corporations in most countries, whereas the high relevance of unincorporated businesses in Germany is rather special (see Sect. 4). However, the effective tax rate on equity invested in unincorporated firms or corporations is very similar in Germany (see footnote 2).

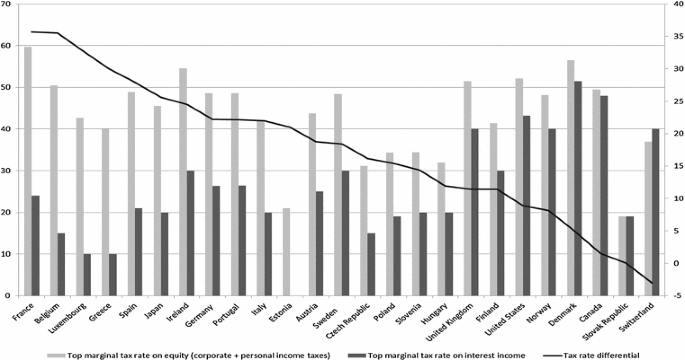

Fig. 1

Top marginal tax rate differences between equity and interest income in selected OECD countries in 2012. Notes: The bars indicate the top marginal tax rates on equity (invested in a corporation, taking into account the corporate and personal taxes) and interest income from the perspective of a personal investor in various OECD countries. The line shows the difference between these two tax rates. The left scale refers to the tax rates, and the right scale to the difference between the tax rates. The tax rates on equity are calculated by assuming full distribution (cf. “old view” of dividend taxation). In Norway, we assume that the rate of return exceeds the rate of return allowance. For further details on single countries, see OECD (2013). Sources: Authors’ illustration based on OECD (2013) and German Federal Ministry of Finance (2013)

For a comparison of interest rates, we refer to the return of corporate bonds instead of deposits because of their comparable level of risk. Figure A.1 in the supplementary material shows the distribution of interest rates paid by companies in the sample used in this analysis and the average corporate bond yields for the years 2006–2010. The interest rate paid by the median firm is similar to corporate bond yields in 2008 and 2009, the period of our main analysis, which suggests that the interest rate spread for firms is not very large in Germany.

In Graham (1999), the estimated coefficient is negative, because the tax rate differential is defined as the tax rate on interest income minus the tax rate on equity returns.

A saver’s tax allowance applies for capital income, which we do not consider to be relevant for marginal decisions of most business owners because it is quite low: The tax-exempt amount of annual interest and dividend income and capital gains (before 2009, capital gains were taxable only if a security was held for less than 1 year) was €750 per person in 2007 and 2008 and €801 since 2009; the allowance doubles for married joint filers.

The coalition agreement for the newly forming grand coalition government signed in November 2005 stated the general intention to implement a business tax reform, which was then discussed in broad terms during 2006. A first draft bill was presented in February 2007 and, in July 2007, the law passed the two legislative bodies Bundestag and Bundesrat.

Before 2009, the tax rate on dividends was calculated as corporate tax \(+\) solidarity surcharge \(+\) local business tax \(+\)50 % dividend taxation rule for the PIT (shareholder-relief system); the last summand was replaced by the final withholding tax on the full dividend in 2009, which yields a similar tax rate for shareholders in the top PIT bracket.

The uniform basic tax rate was reduced from 0.05 to 0.035 on January 1, 2008, along with other changes that partly offset this tax rate reduction. The local business tax is mostly a tax on profits, although some additions and reductions apply, e.g., financing expenses are partly added back to the local business tax base. The firm’s location, not the owners’ location of residence, is relevant to determine the tax rate. For companies operating in multiple municipalities, the total tax base is distributed according to an apportionment formula, and each municipality applies its multiplier to its allocated share. As we can only observe a company’s registered office, we can only use the multiplier associated with this location.

In an e-mail on November 7, 2014, Frank Hechtner at Freie Universität Berlin reported that less than half a percent of all partners of partnership firms (without liberal professionals) in Germany made use of the preferential tax rules for retained earnings in 2008, according to the official personal income tax statistics for 2008, which are provided by the Statistical Offices. The share among the liberal professionals (e.g., law firms) is even smaller by an order of magnitude, according to the same source.

The variation in local business tax rates is used in the second approach only.

In fact, 42,361 of the 46,285 partnership firms in our sample observed in 2008 have a personal ownership share of more than 99 %, and 2718 are almost exclusively owned by corporations.

To improve the matching quality further, we add squared and cubed terms as well as interaction terms of some variables (see Table A 1 in the supplementary material).

As bandwidth parameter, we follow Heckman et al. (1997) and choose 0.06.

This removes 292 of the 46,285 observations in the sample used in the main specifications.

The results do not change when we use an IV approach instead, where we include the potentially endogenous changes of these two control variables between 2008 and 2009 and use the twice-lagged levels as their IVs. In the specifications including the change in the ratio EBITDA/total assets, we also use its twice-lagged level as its IV, as it might be endogenous as well.

The instrument for the change in the tax rate differential is calculated in the same way in all the years, analogous to what we describe above for the change between 2008 (period \(t-1\)) and 2009 (period \(t\)), i.e., we use the twice-lagged shareholder structure (\(\alpha _{ji,t-2}\)) to simulate the first differenced tax rate differentials \(\tau _{it}^{\mathrm{diff,IV}} - \tau _{i,t-1}^{\mathrm{diff,IV}}\) that we use as IV.

Corporations have to publish their financial statements according to §325 German Commercial Code. The same publication requirements apply also to unincorporated firms with limited liability such as the legal form GmbH & Co. KG, which is explained further below.

The introduction of the final withholding tax in 2009 was also somewhat more complicated for corporations than for partnerships. First, the shareholder-relief system for dividends was replaced with the final withholding tax (although this did not change the effective tax burden for shareholders in the highest PIT bracket, see footnote 9). Second, capital gains, which before 2009 were tax exempt when the equity was held for more than a year, became subject to the new final withholding tax if the equity was acquired on or after January 1, 2009.

Using time series data for 1900–1939, Goolsbee (1998) finds only small effects of taxes on the organizational form, whereas in Goolsbee (2004), he reports much larger effects based on cross-sectional data. Thoresen and Alstadsaeter (2008) find that the introduction of a Dual Income Tax increases the probability of incorporation for an active owner of a human capital intensive business.

In two robustness checks, we require that 60 % (90 %, resp.) of the shareholders structure be observed. The results do not change significantly.

In the robustness section, we alternatively explore three different indicators of debt usage, (i) the ratio of long-term liabilities/total assets; (ii) log total liabilities; and (iii) interest expenses. Our notion of debt does not include pension commitments, which play a minor role in Germany because of the statutory pension insurance system. It does contain non-interest-bearing liabilities such as trade payables.

While the histograms only show the range between \(-\)0.2 and 0.2, we inspected the complete distribution. There are no more peaks or major differences between the two groups of firms outside of this range.

It is unlikely that the local treatment effect identified in our IV estimation differs from the global effect because of the few changes in the shareholder structure.

It is not feasible to additionally include the endogenous first difference of the cash flow, instrumented with its second lag, because the instruments become very weak, presumably due to the high correlation between EBITDA and the cash flow.

Both, in specifications (B9) and (B10), the estimated coefficient of the tax rate differential increases when we choose higher thresholds to cut off outliers. Thus, by choosing 25 % growth as the cutoff level, we are being conservative.

As the change in the tax rate differential is treated as endogenous in the IV estimation, changes in its interaction terms are also endogenous. Therefore, the changes in the interactions of the IV for the tax rate differential are used as additional instruments. First-stage statistics for the changes in the industry dummy interactions are satisfactory (available from the authors on request). First-stage statistics for the other specifications are provided at the bottom of the table.

Since investment might be endogenous, we additionally use an IV approach to assess robustness. As the excluded instrument for an individual firm’s investment quota, we use the average investment quota of all firms within the same 3-digit industry in the same year (without the firm’s own investment quota). The coefficient of the interaction term is positive and significant again (1.10 with a standard error of 0.332). We report the OLS results in the table because the first-stage statistics do not sufficiently support the strength of the instrument for investment.

References

Almeida, H., & Campello, M. (2007). Financial constraints, asset tangibility, and corporate investment. Review of Financial Studies, 20(5), 1429–1460.

Alworth, J., & Arachi, G. (2001). The effect of taxes on corporate financing decision: Evidence from a panel of Italian firms. International Tax and Public Finance, 8, 353–376.

Auerbach, A. J. (2002). Taxation and corporate financial policy. In A. Auerbach & M. Feldstein (Eds.), Handbook of public economics (Vol. 3, pp. 1251–1292). Amsterdam: Elsevier North-Holland.

Bang, H., & Robbins, J. (2005). Doubly robust estimation in missing data and causal inference models. Biometrics, 61(4), 962–972.

Binsbergen, V., Jules, H., Graham, J., & Yang, J. (2010). The cost of debt. Journal of Finance, 65(6), 2089–2136.

Bradley, M., Jarrell, G. A., & Han Kim, E. (1984). On the existence of an optimal capital structure: Theory and evidence. Journal of Finance, 39(3), 857–878.

Bundesbank. (2014). Umlaufsrenditen inländischer Inhaberschuldverschreibungen/Anleihen von Unternehmen (Return on domestic bonds payable to bearer/corporate bonds) http://www.bundesbank.de/Navigation/DE/Statistiken/Zeitreihen_Datenbanken/Makrooekonomische_Zeitreihen/its_list_node.html?listId=www_s140_it01, last accessed June 26, 2014.

Buslei, H., & Simmler, M. (2012). The impact of introducing an interest barrier—Evidence from the German corporation tax reform 2008, DIW Discussion Paper, 1215, German Institute for Economic Research.

Caliendo, M., & Kopeinig, S. (2008). Some practical guidance for the implementation of propensity score matching. Journal for Economic Surveys, 22(1), 31–72.

Chan, H., Faff, R., & Ramsay, A. (2005). Firm size and information content of annual earnings announcements: Australian evidence. Journal of Business Finance and Accounting, 32, 211–253.

Chetty, R., & Saez, E. (2006). The effects of the 2003 dividend tax cut on corporate behavior: Interpreting the evidence. American Economic Review, 96(2), 124–129.

DeAngelo, H., & Masulis, R. W. (1980). Optimal capital structure under taxation. Journal of Financial Economics, 8, 3–29.

DeAngelo, H., DeAngelo, L., & Stulz, R. M. (2006). Dividend policy and the earned/contributed capital mix: A test of the life-cycle theory. Journal of Financial Economics, 81(2), 227–254.

Devereux, M. P., Lockwood, B., & Redoano, M. (2008). Do countries compete over corporate tax rates? Journal of Public Economics, 92(5–6), 1210–1235.

Dwenger, N., & Steiner, V. (2014). Financial leverage and corporate taxation: Evidence from German corporate tax return data. International Tax and Public Finance, 21(1), 1–28.

Farrar, D. E., & Selwyn, L. L. (1967). Taxes, corporate financial policy and return to investors. National Tax Journal, 20, 444–454.

Fazzari, S. M., Glenn Hubbard, R., & Petersen, B. C. (1988). Financing constraints and corporate investment. Brookings Papers on Economic Activity, 19(1), 141–195.

Fazzari, S. M., Glenn Hubbard, R., & Petersen, B. C. (2000). Investment-cash flow sensitivities are useful: A comment on Kaplan and Zingales. Quarterly Journal of Economics, 115(2), 695–705.

Federal Statistical Office. (2011). Umsatzsteuerstatistik 2009 (VAT statistics 2009), Wiesbaden, Germany.

Feld, L. P., Heckemeyer, J. H., & Overesch, M. (2013). Capital structure choice and company taxation: A meta-study. Journal of Banking and Finance, 37(8), 2850–2866.

Fossen, F. M., & Bach, S. (2008). Reforming the German local business tax—Lessons from an international comparison and a microsimulation analysis. FinanzArchiv: Public Finance Analysis, 64(2), 245–272.

Fuest, C., Huber, B., & Nielson, S. B. (2002). Why is the corporate tax rate lower than the personal tax rate? The role of new firms. Journal of Public Economics, 87, 157–174.

Fuest, C., & Weichenrieder, A. (2002). Tax competition and profit shifting: On the relationship between personal and corporate tax rates. IFO-Studien, 48, 611–632.

German Council of Economic Experts. (2006). Reform der Einkommens- und Unternehmensbesteuerung in Deutschland durch die Duale Einkommensteuer (Reform of income and business taxation in Germany by way of the Dual Income Tax). Wiesbaden: Statistisches Bundesamt.

German Federal Ministry of Finance. (2013). Die wichtigsten Steuern im internationalen Vergleich 2012, Ausgabe 2013 (The most important taxes in international comparison in 2012, edition of 2013), Berlin, Germany.

Goolsbee, A. (1998). Taxes, organizational form, and the deadweight loss of the corporate income tax. Journal of Public Economics, 69, 143–152.

Goolsbee, A. (2004). The impact of the corporate income tax: Evidence from state organizational form data. Journal of Public Economics, 88, 2283–2299.

Gordon, R. H., & MacKie-Mason, J. K. (1990). Effects of the Tax Reform Act of 1986 on corporate financial policy and organizational form. In J. Slemrod (Ed.), Do taxes matter? (pp. 91–131). Cambridge: MIT Press.

Gordon, R. H., & MacKie-Mason, J. K. (1994). Tax distortions to the choice of organizational form. Journal of Public Economics, 55(2), 279–306.

Gordon, R. H., & Gaspar, V. (2001). Home bias in portfolios and taxation of asset income. Advances in Economic Analysis & Policy, 1, 1–30.

Gordon, R. H., & Lee, Y. (2001). Do taxes affect corporate debt policy? Evidence from U.S. corporate tax return data. Journal of Public Economics, 82, 195–224.

Gordon, R. H. (2004). Taxation of interest income. International Tax and Public Finance, 11, 5–15.

Gordon, R. H. (2010). Taxation and corporate use of debt: Implications for tax policy. National Tax Journal, 63, 151–174.

Graham, J. R. (1999). Do personal taxes affect corporate financing decisions? Journal of Public Economics, 73, 147–185.

Graham, J. R. (2003). Taxes and corporate finance: A review. Review of Financial Studies, 16, 1075–1129.

Harris, M., & Raviv, A. (1991). The theory of capital structure. Journal of Finance, 46, 297–355.

Heckman, J., Ichimura, H., & Todd, P. E. (1997). Matching as an econometric evaluation estimator: Evidence from evaluating a job training programme. Review of Economic Studies, 64(4), 605–654.

Hovakimian, A., Opler, T., & Titman, S. (2001). The debt-equity choice. Journal of Financial and Quantitative Analysis, 36(1), 1–24.

Jacob, M., & Jacob, M. (2013). Taxation, dividends, and share repurchases: Taking evidence global. Journal of Financial and Quantitative Analysis, 48(4), 1241–1269.

Kessler, W., Pfuhl, A., & Grether, B. (2011). Die Thesaurierungsbegünstigung nach § 34a EStG in der steuerlichen (Beratungs-)Praxis - Ergebnisse einer onlinebasierten Umfrage (The preferential treatment of retained earnings according to § 34a of the Income Tax Law in tax advisory practice - Results from an online survey). Der Betrieb, 64(4), 185–189.

Kiesewetter, D., & Lachmund, A. (2004). Wirkungen einer Abgeltungsteuer auf Investitionsentscheidungen und Kapitalstruktur von Unternehmen (Effects of a flat rate tax on investment decisions and capital structure of companies). Die Betriebswirtschaft - Business Administration Review, 64(4), 395–411.

Kraemer, R. (2012). Taxation and capital structure choice: The role of ownership. Working paper available at the 2012 IIPF conference website https://editorialexpress.com/cgi-bin/conference/download.cgi?db_name=IIPF68&paper_id=200, last accessed June 26, 2014.

Kraus, A., & Litzenberger, R. H. (1973). A state preference model of optimal financial leverage. Journal of Finance, 28(4), 911–922.

Miller, M. H. (1977). Debt and taxes. Journal of Finance, 32(2), 261–275.

OECD. (2013). OECD tax database, http://www.oecd.org/tax/tax-policy/tax-database.htm, last accessed November 4, 2013.

Overesch, M., & Voeller, D. (2010). The impact of personal and corporate taxation on capital structure choices. Finanzarchiv: Public Finance Analysis, 66(3), 263–294.

Rajan, R. G., & Zingales, L. (1995). What do we know about capital structure? Some evidence from international data. Journal of Finance, 50, 1421–1460.

Rosenbaum, P. R., & Rubin, D. B. (1985). Constructing a control group using multivariate matched sampling methods that incorporate the propensity score. American Statistician, 39, 33–38.

Rottmann, H., & Wollmershäuser, T. (2013). A micro data approach to the identification of credit crunches. Applied Economics, 45(17), 2423–2441.

Schmidt, T., & Zwick, L. (2012). In search for a credit crunch in Germany, Ruhr Economic Papers 361, Rheinisch-Westfälisches Institut für Wirtschaftsforschung (RWI).

Scott, J. H. (1976). A theory of optimal capital structure. Bell Journal of Economics, 7(1), 33–54.

Sørensen, P. B. (1994). From the Global Income Tax to the Dual Income Tax: Recent tax reforms in the Nordic countries. International Tax and Public Finance, 1(1), 57–79.

Statistical Offices of the Federation and the States. (2004–2010). Statistik local (Local statistics), Wiesbaden, Germany.

Thoresen, T. O., & Alstadsaeter, A. (2008). Shifts in organizational form under a Dual Income Tax system. FinanzArchiv: Public Finance Analysis, 66(4), 384–418.

Acknowledgments

We thank Bob Chirinko (the editor), three anonymous referees, Mohamed Belhaj, Jochen Bigus, Jennifer Blouin, Steve Bond, Thies Buettner, Timothy J. Goodspeed, Peter Haan, Frank Hechtner, Henriette Houben, Jochen Hundsdoerfer, Adam Lederer, Søren Bo Nielsen, Uwe Scheuering, Viktor Steiner, as well as participants at the 2012 Congress of the European Economic Association (EEA) in Malaga, the 2012 Congress of the International Institute of Public Finance (IIPF) in Dresden, the 2012 Annual Symposium at the Oxford University Centre for Business Taxation, the 2012 Journées d’Economie Publique Louis-André Gérard-Varet in Marseille, and seminars at Freie Universität Berlin and DIW Berlin, for helpful and valuable comments. Frank Fossen conducted part of this project as a visiting researcher at the University of California, Santa Cruz. He thanks the Fritz Thyssen Foundation for financial support of this research visit.

Author information

Authors and Affiliations

Corresponding author

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Fossen, F.M., Simmler, M. Personal taxation of capital income and the financial leverage of firms. Int Tax Public Finance 23, 48–81 (2016). https://doi.org/10.1007/s10797-015-9349-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-015-9349-0