Abstract

We consider a mixed duopoly selling to downstream retailers that are engaged in spatial price discrimination. We show that the optimal degree of privatization falls below—often far below—the level that is implied in the absence of the vertical chain. The size of this reduction in privatization reflects the extent to which increasing transport cost (differentiation) increases double marginalization in contested market regions—as opposed to simply reducing demand in uncontested market regions. Moreover, we show that despite higher costs of production, a fully public monopoly upstream can be welfare-superior to the optimal mixed duopoly. This would not be the case in the absence of downstream differentiation.

Similar content being viewed by others

Notes

See Heywood and Ye (2009a) for a model in which a public firm competes in a model of spatial price discrimination but without a vertical chain.

It can be verified that it is the difference between upstream firms’ costs that critically influences the model, and so we assume a cost of zero for the private producer.

We can, however, demonstrate that many of the crucial relationships that we prove with these fixed locations can be replicated with alternative assumptions such as assuming that the two downstream firms locate at the traditional quartiles. Yet, we cannot address issues of spatial agglomeration or dispersion that are often of interest (Matsumura et al. 2005).

We recognize that the upstream price could be above zero but less than or equal to \(c_{1}\). This still represents an elevation of upstream price over the minimal possible production cost due to imperfect market structure. This elevated price is built into the subsequent pricing downstream.

This equality flows from the linear demand with a slope of minus one and the fixed downstream mark-up. As there is no upstream production cost, maximization of firm B's revenue results in the equality of price and quantity as it would for a simple revenue-maximizing monopolist.

This equality again reflects the linear demand curve but now with a fully uncontested market. Here the price slope becomes ½, and the fixed downstream markup of \(\frac{\omega }{2}\) equals \(Q_{b}\) under profit maximization by the upstream private firm.

To guarantee an interior solution for the optimal privatization level, we assume \(0 < c_{1} \le 0.2 \equiv \bar{c}_{1}\). The existence of an interior solution for the optimal upstream production further requires \(c_{1} \ge 0.146 \equiv \underset{\raise0.3em\hbox{$\smash{\scriptscriptstyle-}$}}{c}_{1}\). Therefore, we assume \(\underset{\raise0.3em\hbox{$\smash{\scriptscriptstyle-}$}}{c}_{1} \le c_{1} \le \bar{c}_{1}\).

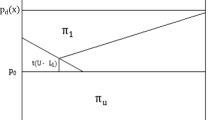

\(t_{T}\) is obtained via solving \(\{ t:x_{1} (\omega^{l*} ,\lambda^{l*} ) = x_{2} (\omega^{l*} ,\lambda^{l*} ) = \frac{1}{2}\}\): No contested regime exists. See Fig. 1.

\(t^{s*}\) is obtained via solving \(\{ t:x_{1} (\omega^{s*} ,\lambda^{s*} ) = 0\}\), or \(\{ t:x_{2} (\omega^{s*} ,\lambda^{s*} ) = 1\}\): The uncontested regime is just about to emerge. See Fig. 1.

In an alternative derivation, we replaced the private domestic upstream firm with a private foreign upstream firm. The profit of the foreign firm is not counted in domestic welfare. We found that optimal privatization (from maximizing domestic welfare) always increases with t. As t increases, downstream firms can set unconstrained prices over larger areas. This increase in price decreases the quantity that is sold and the profit of the upstream foreign firm that leaves the country. Therefore, a mixed firm that maximizes domestic welfare has less incentive to produce more to squeeze the foreign firm’s profit. Thus, the optimal level of privatization increases in t. This showing is available upon request.

It can be proven that there is no incentive to partially privatize an upstream public monopolist.

Thus, any increased marginalization downstream (t > 0) immediately causes the public monopoly to produce more, and thus to price below cost. This contrasts with the optimal mixed oligopoly, which started with price above cost to expand private firm output.

References

Belleflamme, P., & Peitz, M. (2010). Industrial organization: Markets and strategies. Cambridge: Cambridge University Press.

Bortolotti, B., Fantini, M., & Siniscalco, D. (2003). Privatization around the world: Evidence from panel data. Journal of Public Economics, 88, 305–322.

Bowley, A. (1924). The mathematical groundwork of economics. Oxford: Oxford University Press.

Cellini, R., & Lambertini, L. (2009). The make or buy choice in a mixed oligopoly: A theoretical investigation. In L. Lambertini (Ed.), Firms’ objectives and internal organization in a global economy. London: Palgrave Macmillan UK.

Cournot, A. A. (1838). Researches into the mathematical principles of the theory of wealth, English translation by N.T. Bacon reprinted with notes by I. Fisher, New York: Macmillan 1927.

Fjell, K., & Pal, D. (1996). A mixed oligopoly in the presence of foreign private firms. Canadian Journal of Economics, 29, 737–743.

Florio, M. (2014). The return of public enterprise. Working Paper Series. Centre for Industrial Studies, University of Milan 2014/01.

Fujiwara, K. (2007). Partial privatization in a differentiated mixed oligopoly. Journal of Economics, 92, 51–65.

Gelves, J. A., & Heywood, J. S. (2013). Privatizing by merger: The case of an inefficient public leader. International Review of Economics and Finance, 27, 69–79.

Greenhut, M. L. (1981). Spatial pricing in the United States, West Germany and Japan. Economica, 48(189), 79–86.

Gupta, B., Katz, A., & Pal, D. (1994). Upstream monopoly, downstream competition and spatial price discrimination. Regional Science and Urban Economics, 24, 529–542.

Hamilton, J. H., Thisse, J. F., & Weskamp, A. (1989). Spatial discrimination: Bertrand vs. Cournot in a model of location choice. Regional Science and Urban Economics, 19, 87–102.

Heywood, J. S., Wang, S., & Ye, G. (2018). Resale price maintenance and spatial price discrimination. International Journal of Industrial Organization, 57, 147–174.

Heywood, J. S., & Ye, G. (2009a). Mixed oligopoly, sequential entry and spatial price discrimination. Economic Inquiry, 47, 589–597.

Heywood, J. S., & Ye, G. (2009b). Partial privatization in a mixed oligopoly with an R&D rivalry. Bulletin of Economic Research, 61, 165–178.

Heywood, J. S., & Ye, G. (2010). Optimal privatization in a mixed duopoly with consistent conjectures. Journal of Economics, 101, 231–246.

Hsu, C. C. (2016). Partial privatization in upstream mixed oligopoly with free entry. Modern Economy, 7, 1444–1454.

Johnson, C. (Ed.). (1987). Business Strategy and Retailing. New York: Wiley.

Lee, S. H., Nakamura, T., & Park, C. H. (2017). Optimal privatization policy in a mixed eco-industry in the presence of commitments on abatement technologies. Working Paper, Munich Personal RePEc Archive, 80902.

Matsumura, T. (1998). Partial privatization in mixed duopoly. Journal of Public Economics, 70(3), 473–483.

Matsumura, T., & Kanda, O. (2005). Mixed oligopoly at free entry markets. Journal of Economics, 84, 27–48.

Matsumura, T., & Matsushima, N. (2004). Endogenous cost differentials between public and private enterprises: A mixed duopoly approach. Economica, 71, 671–688.

Matsumura, T., Ohkawa, T., & Shimizu, D. (2005). Partial agglomeration or dispersion in spatial Cournot competition. Southern Economic Journal, 72, 224–235.

Matsumura, T., & Tomaru, Y. (2015). Mixed duopoly, location choice, and shadow cost of public funds. Southern Economic Journal, 82, 416–429.

Megginson, W. L., & Netter, J. M. (2001). From state to market: A survey of empirical studies of privatization. Journal of Economic Literature, 39, 321–389.

Pal, D. (1998). Endogenous timing in a mixed oligopoly. Economics Letters, 61, 181–185.

Pal, R., & Saha, B. (2015). Pollution tax, partial privatization and environment. Resource and Energy Economics, 40, 19–35.

Sato, S. & Matsumura, T. (2017). Shadow cost of public funds and privatization policies. Munich Personal RePEc Archive, Working Paper No. 81054.

Sato, S., & Matsumura, T. (2018). Dynamic privatization policy. Manchester School, Forthcoming. https://doi.org/10.1111/manc.12217.

Shaffer, G. (1991). Slotting allowances and resale price maintenance: A comparison of facilitating practices. Rand Journal of Economics, 22, 120–135.

Spengler, J. (1950). Vertical integration and antitrust policy. Journal of Political Economy, 58, 347–352.

Thisse, J. F., & Vives, X. (1988). On the strategic choice of spatial price policy. American Economic Review, 78, 122–137.

Wang, L. F. S., & Chen, T. L. (2011). Mixed oligopoly, optimal privatization, and foreign penetration. Economic Modelling, 28, 1465–1470.

Wang, L. F. S., & Mukherjee, A. (2012). Undesirable competition. Economics Letters, 114, 175–177.

Waterman, D., & Weiss, A. A. (1996). The effects of vertical integration between cable television systems and pay cable networks. Journal of Econometrics, 72, 357–395.

Wu, S. J., Chang, Y. M., & Chen, H. Y. (2016). Imported inputs and privatization in downstream mixed oligopoly with foreign ownership. Canadian Journal of Economics, 49, 1179–1207.

Xu, L. L., Cho, S. M., & Lee, S. H. (2016). Emission tax and optimal privatization in Cournot–Bertrand comparison. Economic Modelling, 66, 73–82.

Yang, Y. P., Wu, S. J., & Hu, J. L. (2014). Market structure, production efficiency, and privatization. Hitotsubashi Journal of Economics, 55, 89–108.

Acknowledgement

Financial support is gratefully acknowledged from the National Natural Science Foundation of China (No. 71773129) and National Social Science Foundation of China (No. 19ZDA110), Changjiang Scholar Program of Chinese Ministry of Education (No. Q2016037).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

1.1 Proof of Proposition 1 for the M-shaped equilibrium

We know that \(\left. {\frac{{\partial W^{m} (\omega^{m*} )}}{\partial \lambda }} \right|_{{\lambda { = }0}}\) reaches its minimum when \(c_{1} = 0.2\) and that the value at the minimum is positive: \(\left. {\frac{{\partial W^{m} (\omega^{m*} )}}{\partial \lambda }} \right|_{{\lambda { = }0}} (c_{1} = 0.2) = 0.1977\). This implies that \(\left. {\frac{{\partial W^{m} (\omega^{m*} )}}{\partial \lambda }} \right|_{{\lambda { = }0}} > 0\) and, therefore, that \(\lambda { = }0\) is never optimal for the M-shaped equilibrium, and that \(\lambda^{m*}\) must be positive.

1.2 Proof of Proposition 2

For the small t of the V-shaped equilibrium (\(0 < t \le t^{s*}\)), we know that \(\omega^{ *} = 2c_{1} - \frac{t}{2}\), so it follows naturally that \(\omega^{ *}\) decreases with t. When \(0 < t \le 2c_{1}\), \(\omega^{*} \ge c_{1}\) and when \(2c_{1} < t \le t^{s*}\), \(\omega^{*} < c_{1}\).

For the moderate t of the M-shaped equilibrium (\(t^{s*} < t \le t^{T}\)), we have \(\omega^{*} (t = t_{T} ) < c_{1} ,\omega^{*} (t = t^{s*} ) < c_{1}\). Further, we show \(\left. {\frac{{\partial \omega^{*} }}{\partial t}} \right|_{{t = t^{s*} }} < 0\), \(\left. {\frac{{\partial \omega^{*} }}{\partial t}} \right|_{{t = t_{T} }} > 0\) and the second derivative of \(\omega^{*}\) with respect to t, \(\frac{{\partial^{2} \omega^{*} }}{{\partial t^{2} }} > 0\) as \(t^{s*} \le t \le t^{T}\). Thus, \(\omega^{*}\) first decreases with t and then increases with t for the M-shaped equilibrium (see "Appendix" Fig. 5).

The optimal wholelsale price under optimal privatization level for the M-shaped equilibrium

Therefore, we have \(\omega^{*} < \omega^{*} (t = t^{s*} ){ = }\omega^{*} (t = t_{T} ) < c_{1}\). In consequence,\(\omega^{ *}\) first decreases with t and then increases with t, and when \(0 < t < 2c_{1}\), \(\omega^{*} > c_{1}\); when \(2c_{1} < t < t_{T}\), \(0 < \omega^{*} < c_{1}\).

1.3 Proof of Proposition 3

When t is small so that only the V-shaped equilibrium exists, the optimal privatization level is \(\lambda^{s*} = \frac{{c_{1} }}{{1 - 4c_{1} + \frac{3t}{4}}}\), and \(\frac{{\partial \lambda^{s*} }}{\partial t} = - \frac{{12c_{1} }}{{(4 + 3t - 16c_{1} )^{2} }} < 0\), therefore \(\lambda^{s*}\) decreases as t increases.

When t becomes larger so that the M-shaped equilibrium exists, the optimal wholesale price becomes:

\({\text{where }}A_{1} = 39\lambda^{2} t^{2} - 4c_{1} \lambda t + 4\lambda^{2} t + 9\lambda t^{2} + 4c_{1}^{2} - 8c_{1} \lambda - 12c_{1} t + 4\lambda^{2} + 16\lambda t - 2t^{2} - 8c_{1} + 8\lambda + 12t + 4\) The FOC of the associated social welfare \(W^{m} (\omega^{m*} )\) with respect to \(\lambda\) yields the optimal privatization level.

While the expression for the optimal privatization level of the M-shaped equilibrium (intermediate values of t) remains very complicated, we can graph it for any \(c_{1}\) (see Fig. 3). Notice that when t is large enough that each firm is uncontested, privatization does not change with t.

We can also show analytically that the optimal privatization level of the M-shaped equilibrium first decreases with t and then increases with t until the upper bound, which is exactly what Proposition 3 indicates.

1.4 Proof of Proposition 4

We denote the optimal privatization level as \(\lambda^{*}\). Since Proposition 3 shows that the optimal privatization level first decreases with t and then increases with t, we have the following inequality:

We have proven in the text that:

So we have: \(\mathop {\hbox{max} }\limits_{t} \lambda^{*} \le \lambda^{s*} (t = 0) = \frac{{c_{1} }}{{1 - 4c_{1} }}\): The optimal privatization level with no double marginalization is the highest, which is what Proposition 4 states.

1.5 Proof of Proposition 5

For small t such that only the contested regime exists downstream the comparison of welfare between a mixed upstream duopoly and a fully public upstream monopoly is: \(W^{s*} (\lambda^{s*} ) - W(\omega^{*} ) = \frac{{c_{1} (3c_{1} - t)}}{2}\).

Recall that for t above \(t^{s*}\) uncontested regimes begin to emerge downstream with mixed upstream duopoly. It is easy to prove that \(t^{s*} < \frac{{2(1 - c_{1} )}}{3}\), the threshold value for t such uncontested regimes begin to appear with the fully public upstream monopolist. Then we have, for \(0 \le t \le \hbox{min} \{ 3c_{1} ,t^{s*} \}\), \(W^{s*} (\lambda^{s*} ) > W(\omega^{*} )\); for \(\hbox{min} \{ 3c_{1} ,t^{s*} \} \le t \le t^{s*}\), \(W^{s*} (\lambda^{s*} ) < W(\omega^{*} )\). Solving \(3c_{1} - t^{s*} = 0\), we have \(c_{1} = 0.154\). Therefore, 1) when \(0.146 < c_{1} < 0.154\), \(W^{s*} (\lambda^{s*} ) > W(\omega^{*} )\) as \(0 \le t \le 3c_{1}\), \(W^{s*} (\lambda^{s*} ) < W(\omega^{*} )\) as \(3c_{1} \le t \le t^{s*}\); 2) when \(0.154 < c_{1} < 0.2\), \(W^{s*} (\lambda^{s*} ) > W(\omega^{*} )\) always holds. So for sufficiently small t, a mixed upstream duopoly yields higher social welfare.

For the large t of \(t_{T}\) such that only uncontested regimes exist with a mixed upstream duopoly, solving \(W^{l*} (\lambda^{l*} ) - W(\omega^{*} ) = 0\) we have \(c_{1} = 0.184\). It is easy to verify that for \(0.146 < c_{1} \le 0.184\), \(W^{l*} (\lambda^{l*} ) < W(\omega^{*} )\); for \(0.184 < c_{1} \le 0.2\), \(W^{l*} (\lambda^{l*} ) > W(\omega^{*} )\). So, for a large t such that uncontested regimes exist, the result of the welfare comparison is ambiguous: It depends on the upstream production cost.

For moderate t such that the M-shaped equilibrium exists, analytic welfare comparisons are intractable. The comparison can be graphed:

"Appendix" Fig. 6 indicates that when \(c_{1}\) is small, the upstream duopoly yields even less social welfare than does monopoly (area I); while when \(c_{1}\) is large, the range of t such that the upstream duopoly yields higher social welfare emerges (area II). Then we know that when \(c_{1}\) is large, the effect of the upstream duopoly’s increasing social welfare is stronger.

Welfare comparison between an upstream duopoly and an upstream monopoly for the M-shaped equilibrium

The discussion above proves Proposition 5.

Rights and permissions

About this article

Cite this article

Heywood, J.S., Wang, S. & Ye, G. Partial Privatization Upstream with Spatial Price Discrimination Downstream. Rev Ind Organ 59, 57–78 (2021). https://doi.org/10.1007/s11151-020-09804-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11151-020-09804-9