Abstract

The paper estimates the dynamic macroeconomic effects of labor and product market reforms on output, employment and productivity, and explores how these vary with prevailing macroeconomic conditions and policies. We apply a local projection method to a new dataset of major country- and country-sector-level reform shocks in various areas of labor market institutions and product market regulation covering 26 advanced economies over the past four decades. Product market reforms are found to raise productivity and output, but gains materialize only slowly. The impact of labor market reforms is primarily on employment, but it varies across types of reforms and depends on overall business cycle conditions—unlike that of product market reforms. Reductions in labor tax wedges and increases in public spending on active labor market policies have larger effects during periods of slack, in part because they usually entail some degree of fiscal stimulus. In contrast, reforms to employment protection arrangements and unemployment benefit systems have positive effects in good times, but can become contractionary in periods of slack. The economy’s response to such reforms is significantly improved when they are accompanied by fiscal or monetary stimulus.

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Source: The authors

Similar content being viewed by others

Notes

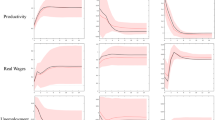

The estimated effects of labor market reforms at a 5-year horizon are roughly in line with those in the literature—including the absence of a significant employment impact of job protection deregulation; see, e.g., Bassanini and Duval (2009). Our estimated impact of product market reforms may be somewhat smaller, although comparisons cannot be readily made. For example, Bourlès and others (2013) find that adopting the lightest regulatory practices observed across advanced economies in each industry would yield a 7.5 percent average GDP gain in advanced economies in the long run. We focus on the much more modest average major historical reform and find a 1.5 percent impact after 5 years (2¼ percent after 7 years).

One exception is when reform is carried out in a situation where monetary policy is constrained by the zero lower bound. Exogenous wage and price markup reductions may then have weaker short-term effects than in normal times (Eggertsson and others 2014).

In this setup, which builds and expands on Blanchard and Giavazzi (2003), cutting regulatory barriers to firm entry increases product variety and shrinks price markups; reducing unemployment benefits weakens workers’ outside option and therefore lowers wages and equilibrium unemployment; and reducing firing costs increases the efficiency of resource allocation across firms in the presence of idiosyncratic productivity shocks—but has an ambiguous effect on unemployment a priori since it increases both job creation and job destruction.

Using a calibrated euro area model with similar theoretical foundations, but using information on more recent (2013) regulatory settings, Cacciatore and others (2016b) find a much smaller steady-state GDP gain of about 2.2 percent for the euro area from converging to US product market regulation.

The 26 countries covered are Australia, Austria, Belgium, Canada, Czech Republic, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Japan, Korea, Luxembourg, the Netherlands, New Zealand, Norway, Portugal, Slovak Republic, Spain, Sweden, Switzerland, UK and United States.

We do not present stylized facts on counter-reforms—that is, increases in regulation—as these are typically rare events in our sample, with the exception for employment protection legislation. In particular, the number of counter-reforms is: (i) 0 for telecommunications, postal services, electricity, gas and road transport; 3 for airline transport; 1 for road transport, 20 for employment protection legislation; and 9 for unemployment benefits.

Results are robust to using instead the forecasts of the spring issue of the same year or the fall issue of the previous year. These are available upon request.

In particular, we first compute the forecast error of the policy rates, proxied by the short-term nominal rate \(\left( {{\text{FE}}_{t}^{i} } \right)\)—defined as the difference between the actual policy rates \(\left( {{\text{ST}}_{t}^{i} } \right)\) and the rate expected by analysts as of October of the same year \(\left( {{\text{CT}}_{t - 1,t}^{i} } \right):{\text{FE}}_{i,t}^{i} = {\text{ST}}_{i,t}^{i} - {\text{CT}}_{i,t - 1,t}^{i}\)—and then regress for each country the forecast errors of the policy rates \(\left( {{\text{ST}}_{t}^{i} } \right)\) on similarly computed forecast errors of inflation \(({\text{FE}}^{ \inf } )\) and output growth \(({\text{FE}}^{g} ):{\text{FE}}_{i,t}^{i} = \alpha + \beta {\text{FE}}_{i,t}^{\inf } + \gamma {\text{FE}}_{i,t}^{g} + \epsilon_{i,t}\) where the residual series—\(\epsilon_{i,t}\)—captures exogenous monetary policy shocks (MP). We use Consensus Economics forecasts rather than the OECD’s Economic Outlook because of the greater country and time coverage of the former.

All reform shocks featured in our database are countrywide shocks, except for product market reform shocks which are constructed at the country-sector level for seven different network industries. For the country-level analysis, the latter are converted into countrywide product market reform shocks as follows. A major reform is considered to take place in country i in year t when at least two out of the seven network industries experience a reform, which in practice corresponds to the 90th percentile of the distribution of the sum of all seven reform dummy variables. Similar results—not reported below but available upon request—are obtained when using the distribution of the weighted sum of the reform dummies instead, with weights equal to the (country-sector specific time-varying) share of value added of each sector in GDP.

The results are robust to different number of lags.

Another advantage of the local projection method compared to vector autoregression (autoregressive distributed lag) specifications is that the computation of confidence bands does not require Monte Carlo simulations or asymptotic approximations. One limitation, however, is that confidence bands at longer horizons tend to be wider than those estimated in vector autoregression specifications.

As noted above, the results are also robust to controlling for future reform shocks, including negative ones (counter-reforms). Furthermore, they do not significantly differ between reforms and counter-reforms, which is why we do not report these separately here.

As reforms in some sectors have been clustered around particular years, we use an industry-specific time trend rather than industry-year fixed effects, as the latter would unduly absorb some of the impact of product market deregulation.

Similar results are obtained using 1996 input–output data instead.

A tentative theoretical rationale for this somewhat surprising finding is provided in Cacciatore and others. (2016b), who highlight the presence of two offsetting factors—which we cannot explore empirically here in the absence of firm-level analysis. On the one hand, compared with normal times, expected profits among prospective entrants are smaller during recessions, which discourage firm entry. On the other hand, the number of competing firms shrinks during recessions, leading to higher profit margins and stimulating firm entry, all else equal.

While our focus is only on reform of regular employment protection, so-called two-tier reforms that relax the protection of temporary contracts without changing that of permanent workers may have a more positive short-term effect even in recessions. This is because such reforms increase incentives to hire (temporary workers) without affecting incentives to lay off—since the protection of regular workers is unchanged, giving rise to a transitory, positive, “honeymoon effect” on employment (Boeri and Garibaldi 2006).

Similar results—albeit somewhat stronger and more statistically significant—are found for the effect of these reforms on unemployment.

There are three possible, non-mutually exclusive explanations for an asymmetric impact of unemployment benefits. First, fiscal multipliers tend to be larger in general during recessions (Auerbach and Gorodnichenko 2012; Blanchard and Leigh 2013; Jordà and Taylor 2013; Abiad and others 2015). This may hold particularly for changes in unemployment benefits, because households also become more credit constrained in downturns (Mian and Sufi 2010). Second, benefit cuts may increase income uncertainty, and therefore precautionary saving, more in recessions than in normal times. Using a heterogeneous-agent model that combines matching frictions in the labor market with incomplete asset markets and nominal rigidities, Ravn and Sterk (2013) show that a reduction in consumption in favor of precautionary saving decreases aggregate demand and firms’ hiring, thereby further weakening demand. Third, recessions may be periods when the number of available jobs tends to be rationed (Landais and others 2015), or periods when hiring is less responsive to benefit policy changes more broadly (Jung and Kuester 2015), although this remains the subject of an intense theoretical and empirical debate.

For product market reforms, no statistically significant difference in impulse responses for output, employment or productivity is found across different macroeconomic policy regimes. For labor tax wedge cuts and increases in public spending on active labor market policies, which often involve a fiscal shock in themselves, there is no case for carrying out this exercise.

A potential concern regarding the analysis is that fiscal shocks may respond to output growth surprises. However, as discussed above, these shocks are only weakly correlated with growth surprises. Moreover, purifying our measure of fiscal shocks by purging it from the portion explained by growth surprises delivers results that are similar to those reported here.

Similar results are found for employment, and when repeating the analysis using public investment shocks—computed similarly to government consumption shocks as the forecast error of government investment to GDP. (See Figure 13 in Appendix).

Table 7 in the Appendix reports the response of output and the smooth transition function to fiscal and monetary policy shocks. It shows that an unexpected 1 percent of GDP increase in government consumption raises output by 0.35 percent and decreases the smooth transition function—which is bounded between 0 (extreme expansion) and 1 (extreme recession)—by 0.04 (that is, 4 percentage points). Likewise, an expansionary monetary policy shock of 100 basis points is found to increase output by 0.30 percent and decrease the smooth transition function by 0.03—that is, 3 percentage points.

Similar results are also obtained for productivity and employment. Furthermore, controlling for major reforms of employment protection legislation for temporary workers, which can be sourced from Duval and others (2018), does not affect our results.

In order to compare these results with those obtained in the baseline, we scale the estimated effect by the average change in the OECD indicator corresponding to our major reform event. For example, in the case of product market regulation we multiply the estimated effect by 0.42, which is the average change in the OECD indicator (of product market regulation in seven non-manufacturing industries, see Koske et al. 2015) when our reform dummy takes value 1.

These results are available upon request.

References

Abiad, Abdul, Davide Furceri, and Petia Topalova. 2015. “The Macroeconomic Effects of Public Investment: Evidence from Advanced Economies.” In IMF Working Paper 15/95. Washington: International Monetary Fund.

Addison, John. 2015. “Collective Bargaining Systems and Macroeconomic and Microeconomic Flexibility: The Quest for Appropriate Institutional Forms in Advanced Economies.” In IZA Discussion Paper No. 9587. Institute for the Study of Labor.

Aghion, Philippe, Philippe Askenazy, Renaud Bourlès, Gilbert Cette, and Nicolas Dromel. 2009. "Education, Market Rigidities and Growth." Economics Letters 102(1): 62–65.

Alesina, A., S. Ardagna, G. Nicoletti, and F. Schiantarelli. 2005. "Regulation and Investment." Journal of the European Economic Association 3(4): 791–825.

Arpaia, Alfonso, Werner Roeger, Janos Varga, and Jan in’t Veld. 2007. “Quantitative Assessment of Structural Reforms: Modeling the Lisbon Strategy.” In European Commission Economic Paper No. 282.

Auerbach, Alan, and Youri Gorodnichenko. 2012. "Measuring the Output Responses to Fiscal Policy." American Economic Journal: Economic Policy 4(2): 1–27.

Auerbach, Alan, and Youri Gorodnichenko. 2013. "Output Spillovers from Fiscal Policy." American Economic Review 103(3): 141–146.

Barone, G., and F. Cingano. 2011. "Service Regulation and Growth: Evidence from OECD Countries." Economic Journal 121(555): 931–957.

Ben Zeev, Nadav, and Evi Pappa. 2014. “Chronicle of a War Foretold: The Macroeconomic Effects of Anticipated Defense Spending Shocks.” In CEPR Discussion Paper 9948. London: Centre for Economic Policy Research.

Bentolila, Samuel, and Giuseppe Bertola. 1990. "Firing Costs and Labour Demand: How Bad is Eurosclerosis?" Review of Economic Studies 57(3): 381–402.

Bassanini, Andrea, and Romain Duval. 2009. "Unemployment, Institutions, and Reform Complementarities: Re-Asessing the Aggregate Evidence for OECD Countries." Oxford Review of Economic Policy 25(1): 40–59.

Bassanini, Andrea, Luca Nunziata, and Danielle Venn. 2009. "Job Protection Legislation and Productivity Growth in OECD Countries." Economic Policy 24(58): 349–402.

Blanchard, Olivier, and Francesco Giavazzi. 2003. "Macroeconomic Effects of Regulation and Deregulation in Goods and Labour Markets." Quarterly Journal of Economics 118(3): 879–907.

Blanchard, Olivier, and Augustin Landier. 2002. "The Perverse Effects of Partial Labour Market Reform: Fixed-Term Contracts in France." The Economic Journal 112(480): 214–244.

Blanchard, Olivier, and Daniel Leigh. 2013. "Growth Forecast Errors and Fiscal Multipliers." American Economic Review: Papers and Proceedings 103(3): 117–120.

Blanchard, Olivier, and Justin Wolfers. 2000. "The Role of Shocks and Institutions in the Rise of European Unemployment: The Aggregate Evidence." The Economic Journal 110(462): 1–33.

Boeri, Tito, Pierre Cahuc, and Andre Zylberberg. 2015. “The Costs of Flexibility-Enhancing Structural Reforms: A Literature Review.” In OECD Economics Department Working Papers No. 1264.

Boeri, Tito, and Pietro Garibaldi. 2006. "Two Tier Reforms of Employment Protection: A Honeymoon Effect?" The Economic Journal 117(521): 357–385.

Boeri, Tito, and Juan Jimeno. 2016. "Learning from the Great Divergence in Unemployment in Europe During the Crisis." Labour Economics 41: 32–46.

Bordon, Anna Rose, Christian Ebeke and Kazuko Shirono. 2016. “When Do Structural Reforms Work? On the Role of the Business Cycle and Macroeconomic Policies.” IMF Working Paper 16/62. Washington: International Monetary Fund.

Bouis, Romain, Orsetta Causa, Lilas Demmou, and Romain Duval. 2012. "How Quickly Does Structural Reform Pay Off? An Empirical Analysis of the Short-term Effects of Unemployment Benefit Reform." IZA Journal of Labor Policy 1(1): 1–12.

Bouis, Romain, and Romain Duval. 2011. “Raising Potential Growth after the Crisis: A Quantitative Assessment of the Potential Gains from Various Structural Reforms in the OECD Area and Beyond.” In OECD Economics Department Working Paper 835. Paris.

Bouis, Romain, Romain Duval, and Johannes Eugster. 2016. “Product Market Deregulation and Growth: New Country-Industry-Level Evidence.” IMF Working Paper 16/62. Washington: International Monetary Fund.

Bourlès, Renaud, Gilbert Cette, Jimmy Lopez, Jacques Mairesse, and Giuseppe Nicoletti. 2013. "Do Product Market Regulations in Upstream Sectors Curb Productivity Growth? Panel Data Evidence for OECD Countries." The Review of Economics and Statistics 95(5): 1750–1768.

Cacciatore, Matteo, Romain Duval, Giuseppe Fiori, and Fabio Ghironi. 2016a. "Short-Term Pain for Long-Term Gain: Market Deregulation and Monetary Policy in Small Open Economies." Journal of International Money and Finance 68(November): 358–385.

Cacciatore, Matteo, Romain Duval, Giuseppe Fiori, and Fabio Ghironi. 2016b. "Market Reforms in the Time of Imbalance." Journal of Economic Dynamics and Control 72: 69–93.

Cacciatore, Matteo, and Giuseppe Fiori. 2016. "The Macroeconomic Effects of Goods and Labor Market Deregulation." Review of Economic Dynamics 20(1): 1–24.

Coenen, Günter, Christopher J. Erceg, Charles Freedman, Davide Furceri, Michael Kumhof, René Lalonde, Douglas Laxton, et al. 2012. "Effects of Fiscal Stimulus in Structural Models." American Economic Journal: Macroeconomics 4(1): 22–68.

Corsetti, Giancarlo, Andre Meier, and Gernot J. Müller. 2012. “What Determines Government Spending Multipliers?” IMF Working Paper 12/150. Washington: International Monetary Fund.

Dabla-Norris, E., S. Guo, V. Haksar, K. Kochhar, K. Wiseman, and A. Zdzienicka. 2015. “The New Normal: A Sector-Level Perspective on Productivity Trends in Advanced Economies.” IMF Staff Discussion Note No. 15/03. Washington: International Monetary Fund.

Devries, Pete, Daniel Leigh, Jaime Guajardo, and Andrea Pescatori. 2011. “A New Action-Based Dataset of Fiscal Consolidation.” IMF Working Paper 11/128. Washington: International Monetary Fund.

Drazen, Allan, and William Easterly. 2001. "Do Crises Induce Reform? Simple Empirical Tests of Conventional Wisdom." Economics and Politics 13(2): 129–157.

Duval, Romain, Davide Furceri, Bingjie Hu, Joao Jalles, and Huy Nguyen. 2018. “A Narrative Database of Product and Labor Market Reforms in Advanced Economies.” IMF Working Paper. Washington: International Monetary Fund.

Eggertsson, Gauti, Andrea Ferrero, and Andrea Raffo. 2014. "Can Structural Reforms Help Europe." Journal of Monetary Economics 61(C): 2–22.

Everaert, Luc, and Werner Schule. 2008. "Why it Pays to Synchronize Structural Reforms in the Euro Area across Markets and Countries." IMF Staff Papers 55(2): 356–366.

Fiori, G., G. Nicoletti, S. Scarpetta, and F. Schiantarelli. 2012. "Employment Outcomes and the Interaction between Product and Labor Market Deregulation: Are They Substitutes or Complements?" Economic Journal 122(558): 79–104.

Forni, Mario, and Luca Gambetti. 2010. “Fiscal Foresight and the Effects of Government Spending.” CEPR Discussion Paper 7840. London: Centre for Economic Policy Research.

Gomes, Sandra, Pierre Jacquinot, Matthias Mohr, and Massimiliano Pisani. 2011. “Structural Reforms and Macroeconomic Performance in the Euro Area Countries: A Model-based Assessment.” ECB Working Paper No. 1323.

Granger, Clive W.J., and Timo Teräsvirta. 1993. Modelling Nonlinear Economic Relationships. New York: Oxford University Press.

International Monetary Fund (IMF). 2016. "Staff Background Paper for G-20 Surveillance Note: Priorities for Structural Reforms in G20 Countries." Washington: IMF Staff Report.

Inklaar, R., M. Timmer, and B. Van Ark. 2008. "Market Services Productivity Growth across Europe and the US." Economic Policy 23(53): 139–194.

Jordà, Òscar. 2005. "Estimation and Inference of Impulse Responses by Local Projections." American Economic Review 95(1): 161–182.

Jordà, Òscar, and Alan Taylor. 2013. “The Time for Austerity: Estimating the Average Treatment Effect of Fiscal Policy.” NBER Working Paper. Cambridge, Massachusetts: National Bureau of Economic Research.

Jung, Philip, and Keith Kuester. 2015. "Optimal Labor-Market Policy in Recessions." American Economic Journal: Macroeconomics 7(2): 124–156.

Kilian, L., and Y.T. Kim. 2011. "How Reliable Are Local Projection Estimators of Impulse Reponses?" Review of Economics and Statistics 93(4): 1460–1466.

Koske, I., I. Wanner, R. Bitetti, and O. Barbiero (2015). "The 2013 Update of the OECD Product Market Regulation Indicators: Policy Insights for OECD and Non- OECD Countries." OECD Economics Department Working Papers No. 1200.

Landais, Camille. 2015. "Assessing the Welfare of Unemployment Benefits using the Regression Kink Design." American Economic Journal: Economic Policy 7(4): 243–278.

Landais, Camille, Pascal Michaillat, and Emmanuel Saez. 2015. “A Theory of Optimal Unemployment Benefit Insurance over the Business Cycle.” NBER Working Paper 16526. Cambridge, Massachusetts: National Bureau of Economic Research.

Leeper, Eric M., Alexander W. Richter, and Todd B. Walker. 2012. "Quantitative Effects of Fiscal Foresight." American Economic Journal: Economic Policy 4(2): 115–144.

Leeper, Eric M., Todd B. Walker, and Shu-Chun S. Yang. 2013. "Fiscal Foresight and Information Flows." Econometrica 81(3): 1115–1145.

Mian, Atif R., and Amir Sufi. 2010. “Household Leverage and the Recession of 2007 to 2009.” NBER Working Paper 15896. Cambridge, Massachusetts: National Bureau of Economic Research.

Nickell, Steven, Luca Nunziata, and Wolfgang Ochel. 2005. "Unemployment in the OECD since the 1960s: What Do We Know?" The Economic Journal 115(500): 1–27.

Nicoletti, G., and S. Scarpetta. 2003. "Regulation, Productivity and Growth: OECD Evidence." Economic Policy 18(36): 9–72.

Organisation for Economic Co-operation and Development (OECD). 2006. “Boosting Jobs and Incomes: The Reassessed Jobs Strategy.” Paris.

Organisation for Economic Co-operation and Development (OECD). 2016. “Economic Policy Reforms: Going for Growth.” Paris.

Prati, Alessandro, Massimiliano Gaetano Onorato, and Chris Papageorgiou. 2013. "Which Structural Reforms Work and Under What Institutional Environment? Evidence from a New Data Set on Structural Reforms." Review of Economics and Statistics 95(3): 946–968.

Perotti, Roberto. 1999. "Fiscal Policy in Good Times and Bad." Quarterly Journal of Economics 114(4): 1399–1436.

Rajan, Raghuram G., and Luigi Zingales. 1998. "Financial Dependence and Growth." American Economic Review 88(3): 559–586.

Ravn, Morten O., and Vincent Sterk. 2013. “Job Uncertainty and Deep Recessions.” In Meeting Paper 921. New York: Society for Economic Dynamics, Stonybrook.

Romer, Christina D., and David H. Romer. 1989. "Does Monetary Policy Matter? A New Test in the Spirit of Friedman and Schwartz." In NBER Macroeconomics Annual 1989, ed. Olivier J. Blanchard, and Stanley Fischer, 121–170. Cambridge: MIT Press.

Romer, Christina D., and David H. Romer. 2004. "A New Measure of Monetary Shocks: Derivation and Implications." American Economic Review 94(4): 1055–1084.

Romer, Christina D., and David H. Romer. 2010. "The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks." American Economic Review 100(3): 763–801.

Romer, Christina D., and David H. Romer. 2015. “New Evidence on the Impact of Financial Crises in Advanced Countries.” NBER Working Paper 21021. Cambridge, Massachusetts: National Bureau of Economic Research.

Tommasi, Mariano, and Andres Velasco. 1996. "Where Are We in the Political Economy of Reform?" Journal of Policy Reform 1(2): 187–238.

Author information

Authors and Affiliations

Corresponding author

Additional information

The views expressed in this paper are those of the authors and do not necessarily reflect those of the IMF, its Executive Board, or IMF management. We would like to thank Olivier Blanchard, Jorg Decressin, Maurice Obstfeld, Gian Maria Milesi-Ferretti, Jonathan Ostry, two anonymous referees, as well as participants to various seminars and conferences at Banca d’Italia, Banco de Espana, Banco de Portugal, Bank of England, Bank of Korea, Banque de France, European Central Bank, European Commission, ILO, IMF and OECD for valuable comments. All remaining errors are ours.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Appendix

Appendix

See Figs. 12, 13, 14 and Table 7.

Source: The authors

Fiscal and monetary policy shocks. a Fiscal policy shocks, b monetary policy shocks.

Source: The authors

Impulse responses to reforms under alternative fiscal policy stances—with fiscal stance measured using public investment shocks. a Employment protection legislation reforms, b unemployment benefit reforms. Note t = 0 is the year of the EPL (UB) reform. Solid blue lines denote the response to reform in periods of fiscal expansion (contraction), and dashed lines denote 90 percent confidence bands. Solid yellow lines denote the unconditional (baseline) response presented in Figure 3 (4). Estimates based on Equation (2) using public investment shocks to compute the fiscal policy regime variable. (Color figure online).

Source: The authors

Output effects of product market reforms—the role of employment protection legislation. Note t = 0 is the year of the PMR reform. Solid blue lines denote the response to reform in countries with high (low) EPL, and dashed lines denote 90 percent confidence bands. Solid yellow lines denote the unconditional (baseline) response presented in Fig. 1.

Rights and permissions

About this article

Cite this article

Duval, R., Furceri, D. The Effects of Labor and Product Market Reforms: The Role of Macroeconomic Conditions and Policies. IMF Econ Rev 66, 31–69 (2018). https://doi.org/10.1057/s41308-017-0045-1

Published:

Issue Date:

DOI: https://doi.org/10.1057/s41308-017-0045-1